Christian Julliard

@christianjulliard.net

I think, read, write, teach (and take photos). Associate Professor @LSEFinance. I study the interaction between financial markets and the macroeconomy.

https://christianjulliard.net

https://christianjulliard.net

🔵 Paper: tinyurl.com/4m733etp

🔵 In 20 Slides: tinyurl.com/yc54pkz5

🔵 Codes & Replication: tinyurl.com/4c5tneh6

n/n - fin

🔵 In 20 Slides: tinyurl.com/yc54pkz5

🔵 Codes & Replication: tinyurl.com/4c5tneh6

n/n - fin

tinyurl.com

June 17, 2025 at 10:04 PM

🔵 Paper: tinyurl.com/4m733etp

🔵 In 20 Slides: tinyurl.com/yc54pkz5

🔵 Codes & Replication: tinyurl.com/4c5tneh6

n/n - fin

🔵 In 20 Slides: tinyurl.com/yc54pkz5

🔵 Codes & Replication: tinyurl.com/4c5tneh6

n/n - fin

Bottom line:

✅ Financial markets help identify the true process of consumption

✅ This helps solve long-standing asset pricing puzzles

✅ Time-varying volatility of consumption? Probably not the main story behind time-varying risk premia

12/n

✅ Financial markets help identify the true process of consumption

✅ This helps solve long-standing asset pricing puzzles

✅ Time-varying volatility of consumption? Probably not the main story behind time-varying risk premia

12/n

June 17, 2025 at 10:04 PM

Bottom line:

✅ Financial markets help identify the true process of consumption

✅ This helps solve long-standing asset pricing puzzles

✅ Time-varying volatility of consumption? Probably not the main story behind time-varying risk premia

12/n

✅ Financial markets help identify the true process of consumption

✅ This helps solve long-standing asset pricing puzzles

✅ Time-varying volatility of consumption? Probably not the main story behind time-varying risk premia

12/n

What about time-varying risk premia?

Contrary to many models, we find no evidence that stochastic volatilities in consumption drive them.

Instead, it’s the (shocks to the) conditional mean of consumption the main link between consumption and returns.

11/n

11/n

June 17, 2025 at 10:04 PM

What about time-varying risk premia?

Contrary to many models, we find no evidence that stochastic volatilities in consumption drive them.

Instead, it’s the (shocks to the) conditional mean of consumption the main link between consumption and returns.

11/n

11/n

We verify these mechanisms with a plethora of perturbations to specification / data / frequencies / etc

No matter how we slice it, the result holds: consumption reacts slowly but strongly to financial shocks, & these slowly propagating shocks command very large risk premia.

10/n

No matter how we slice it, the result holds: consumption reacts slowly but strongly to financial shocks, & these slowly propagating shocks command very large risk premia.

10/n

June 17, 2025 at 10:04 PM

We verify these mechanisms with a plethora of perturbations to specification / data / frequencies / etc

No matter how we slice it, the result holds: consumption reacts slowly but strongly to financial shocks, & these slowly propagating shocks command very large risk premia.

10/n

No matter how we slice it, the result holds: consumption reacts slowly but strongly to financial shocks, & these slowly propagating shocks command very large risk premia.

10/n

Is this Long Run Risk?

Not verbatim, but rather medium run / business cycle risk: consumption reacts to priced shocks fully within 2-3 years.

Hence, priced consumption risk is about what happens within the next business cycle, rather than hundred years down the line.

9/n

Not verbatim, but rather medium run / business cycle risk: consumption reacts to priced shocks fully within 2-3 years.

Hence, priced consumption risk is about what happens within the next business cycle, rather than hundred years down the line.

9/n

June 17, 2025 at 10:04 PM

Is this Long Run Risk?

Not verbatim, but rather medium run / business cycle risk: consumption reacts to priced shocks fully within 2-3 years.

Hence, priced consumption risk is about what happens within the next business cycle, rather than hundred years down the line.

9/n

Not verbatim, but rather medium run / business cycle risk: consumption reacts to priced shocks fully within 2-3 years.

Hence, priced consumption risk is about what happens within the next business cycle, rather than hundred years down the line.

9/n

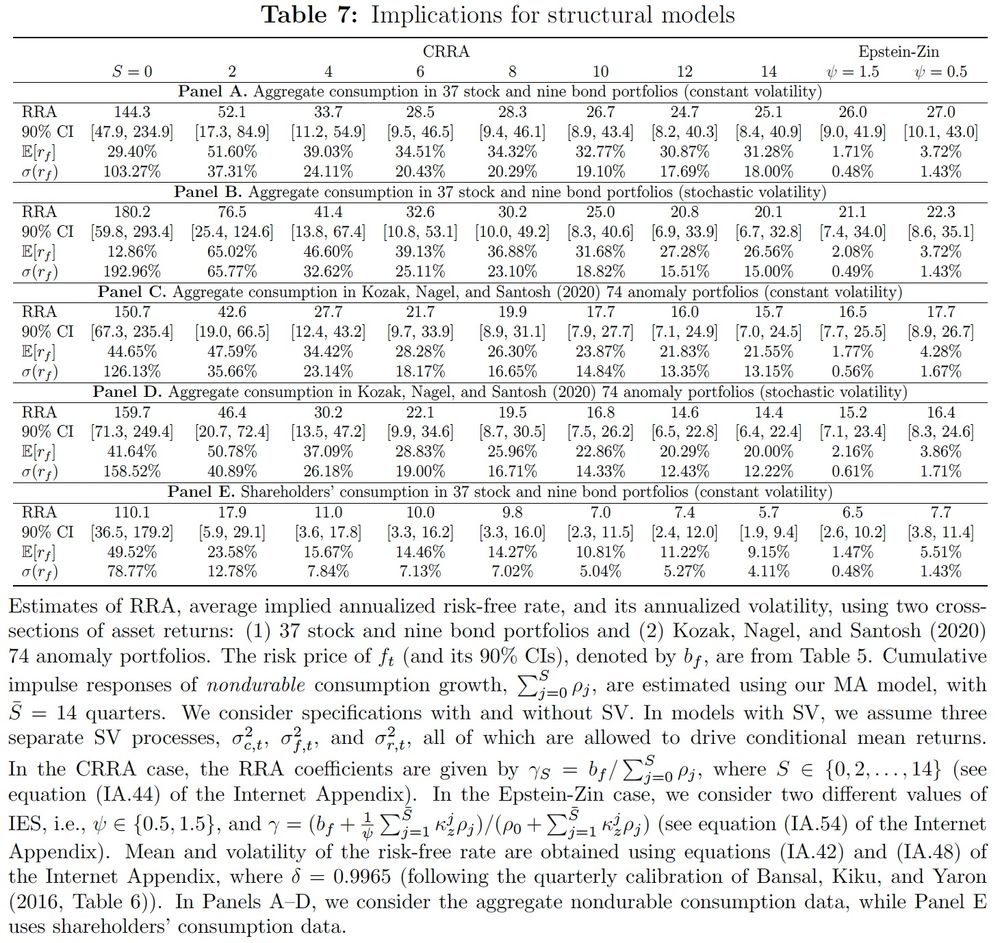

We embed our estimated process into a standard recursive utility model.

With low risk aversion, it explains both the equity premium and the risk-free rate puzzles.

No need for exotic preferences or extreme calibrations.

8/n

8/n

June 17, 2025 at 10:04 PM

We embed our estimated process into a standard recursive utility model.

With low risk aversion, it explains both the equity premium and the risk-free rate puzzles.

No need for exotic preferences or extreme calibrations.

8/n

8/n

To validate our identification, we turn to micro data.

Only stockholders’ consumption responds to financial shocks.

Non-stockholders’ doesn’t. Aggregate consumption sits in between.

Exactly what theory predicts.

7/n

7/n

June 17, 2025 at 10:04 PM

To validate our identification, we turn to micro data.

Only stockholders’ consumption responds to financial shocks.

Non-stockholders’ doesn’t. Aggregate consumption sits in between.

Exactly what theory predicts.

7/n

7/n

These shocks aren’t just statistically significant—they’re economically meaningful. They command an annual Sharpe ratio of ~0.5 (as large as the market!) and explain a large share of stock return variation (and a modest but significant share of bond excess returns too).

6/n

6/n

June 17, 2025 at 10:04 PM

These shocks aren’t just statistically significant—they’re economically meaningful. They command an annual Sharpe ratio of ~0.5 (as large as the market!) and explain a large share of stock return variation (and a modest but significant share of bond excess returns too).

6/n

6/n

Using a flexible state-space model we find that aggregate consumption reacts over multiple quarters to shocks spanned by financial markets, accounting for over 25% of consumption variation.

5/n

5/n

June 17, 2025 at 10:04 PM

Using a flexible state-space model we find that aggregate consumption reacts over multiple quarters to shocks spanned by financial markets, accounting for over 25% of consumption variation.

5/n

5/n

Hence, news about current and future priced consumption states are immediately reflected in prices, and we can use returns to learn about consumption dynamics.

4/n

4/n

June 17, 2025 at 10:04 PM

Hence, news about current and future priced consumption states are immediately reflected in prices, and we can use returns to learn about consumption dynamics.

4/n

4/n

Our identification strategy is grounded in theory:

📌 The Euler equation links consumption and returns

📌 Asset prices are “jump” variables—they react to shocks as they occur

3/n

📌 The Euler equation links consumption and returns

📌 Asset prices are “jump” variables—they react to shocks as they occur

3/n

June 17, 2025 at 10:04 PM

Our identification strategy is grounded in theory:

📌 The Euler equation links consumption and returns

📌 Asset prices are “jump” variables—they react to shocks as they occur

3/n

📌 The Euler equation links consumption and returns

📌 Asset prices are “jump” variables—they react to shocks as they occur

3/n

Most consumption-based asset pricing models rely on “dark matter”--ingredients very powerful in action, yet almost impossible to see with a naked eye or easily verify.

We turn this identification problem on its head: Instead of going from consumption to returns, we go the other way round. 2/n

We turn this identification problem on its head: Instead of going from consumption to returns, we go the other way round. 2/n

June 17, 2025 at 10:04 PM

Most consumption-based asset pricing models rely on “dark matter”--ingredients very powerful in action, yet almost impossible to see with a naked eye or easily verify.

We turn this identification problem on its head: Instead of going from consumption to returns, we go the other way round. 2/n

We turn this identification problem on its head: Instead of going from consumption to returns, we go the other way round. 2/n