Arthur Apostel

@arthurapostel.bsky.social

Econ PhD student at Ghent University. Inequality, tax & climate. https://arthurapostel.github.io/

Pinned

Arthur Apostel

@arthurapostel.bsky.social

· May 26

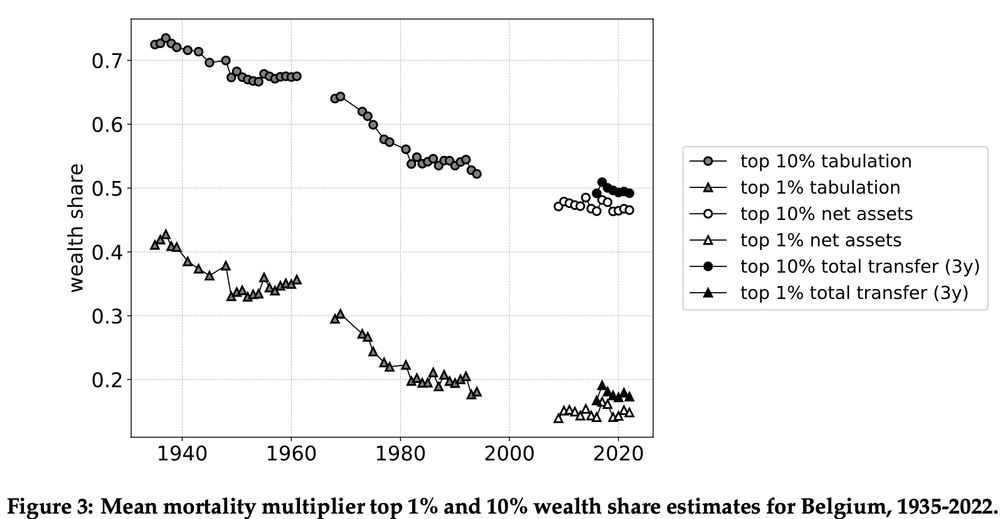

🚨 New working paper: “Belgian wealth inequality, 1935-2022” (NBB WP 477).

▸ Top 1 % owns ≈22 % of net wealth - same as bottom 75 %

▸ Inequality strongly declined last century, stabilised in recent years

PDF 👉 www.nbb.be/en/media/17695

#EconSky #Belgium #WealthInequality

▸ Top 1 % owns ≈22 % of net wealth - same as bottom 75 %

▸ Inequality strongly declined last century, stabilised in recent years

PDF 👉 www.nbb.be/en/media/17695

#EconSky #Belgium #WealthInequality

Hoe zijn de vermogens in België verdeeld? Niet-technische (poging tot toch 😉) blogpost voor de Universitaire Stichting Armoedebestrijding.

Link: blog.uantwerpen.be/armoede-soci...

Link: blog.uantwerpen.be/armoede-soci...

Belgische vermogensongelijkheid, 1935-2022 - Armoede en Sociale Uitsluiting

Hoe is vermogen in België verdeeld? En hoe evolueerde de vermogensverdeling door de tijd heen? In deze blogpost bespreekt Arthur Apostel hoe deze vragen beantwoord kunnen worden en wat de resultaten z...

blog.uantwerpen.be

June 4, 2025 at 11:05 AM

Hoe zijn de vermogens in België verdeeld? Niet-technische (poging tot toch 😉) blogpost voor de Universitaire Stichting Armoedebestrijding.

Link: blog.uantwerpen.be/armoede-soci...

Link: blog.uantwerpen.be/armoede-soci...

Reposted by Arthur Apostel

New study by @arthurapostel.bsky.social (

of Belgian wealth inequality 1935-2022. Findings align with broader European trends: a marked decline over the 20th C, with levels remaining historically low today.

@nbb-bnb-fr.bsky.social

Link to paper: nbb.be/fr/media/17695

of Belgian wealth inequality 1935-2022. Findings align with broader European trends: a marked decline over the 20th C, with levels remaining historically low today.

@nbb-bnb-fr.bsky.social

Link to paper: nbb.be/fr/media/17695

May 26, 2025 at 7:14 PM

New study by @arthurapostel.bsky.social (

of Belgian wealth inequality 1935-2022. Findings align with broader European trends: a marked decline over the 20th C, with levels remaining historically low today.

@nbb-bnb-fr.bsky.social

Link to paper: nbb.be/fr/media/17695

of Belgian wealth inequality 1935-2022. Findings align with broader European trends: a marked decline over the 20th C, with levels remaining historically low today.

@nbb-bnb-fr.bsky.social

Link to paper: nbb.be/fr/media/17695

🚨 New working paper: “Belgian wealth inequality, 1935-2022” (NBB WP 477).

▸ Top 1 % owns ≈22 % of net wealth - same as bottom 75 %

▸ Inequality strongly declined last century, stabilised in recent years

PDF 👉 www.nbb.be/en/media/17695

#EconSky #Belgium #WealthInequality

▸ Top 1 % owns ≈22 % of net wealth - same as bottom 75 %

▸ Inequality strongly declined last century, stabilised in recent years

PDF 👉 www.nbb.be/en/media/17695

#EconSky #Belgium #WealthInequality

May 26, 2025 at 5:52 PM

🚨 New working paper: “Belgian wealth inequality, 1935-2022” (NBB WP 477).

▸ Top 1 % owns ≈22 % of net wealth - same as bottom 75 %

▸ Inequality strongly declined last century, stabilised in recent years

PDF 👉 www.nbb.be/en/media/17695

#EconSky #Belgium #WealthInequality

▸ Top 1 % owns ≈22 % of net wealth - same as bottom 75 %

▸ Inequality strongly declined last century, stabilised in recent years

PDF 👉 www.nbb.be/en/media/17695

#EconSky #Belgium #WealthInequality

Reposted by Arthur Apostel

🚨 New working paper 🚨

I investigate wealth mobility in the United States using data from the Panel Study of Income Dynamics (PSID).

#EconSky #WealthMobility

I investigate wealth mobility in the United States using data from the Panel Study of Income Dynamics (PSID).

#EconSky #WealthMobility

January 30, 2025 at 1:48 PM

🚨 New working paper 🚨

I investigate wealth mobility in the United States using data from the Panel Study of Income Dynamics (PSID).

#EconSky #WealthMobility

I investigate wealth mobility in the United States using data from the Panel Study of Income Dynamics (PSID).

#EconSky #WealthMobility

Reposted by Arthur Apostel

Hot off the press by @margitschratz.bsky.social: A review article on the behavioural responses to inheritance taxation. Some takeaways: Real responses are smaller than avoidance, responses are smaller in more recent studies, tax design matters, ... worth a read: www.sciencedirect.com/science/arti...

Behavioral Responses to Inheritance Taxation – A Review of the Empirical Literature

Increasing wealth inequality and concentration, together with the search for options to secure long-term sufficiency of tax systems in face of ageing …

www.sciencedirect.com

December 4, 2024 at 9:15 PM

Hot off the press by @margitschratz.bsky.social: A review article on the behavioural responses to inheritance taxation. Some takeaways: Real responses are smaller than avoidance, responses are smaller in more recent studies, tax design matters, ... worth a read: www.sciencedirect.com/science/arti...

Reposted by Arthur Apostel

📯 Job Market Paper Alert 📯

Private businesses make up 50% of sales & profits and are the main wealth component of the wealthiest households. So, what is their value? Well, that's difficult, since they're not listed: their value is unobservable by definition!

My #EconJMP tackles this problem 1/

Private businesses make up 50% of sales & profits and are the main wealth component of the wealthiest households. So, what is their value? Well, that's difficult, since they're not listed: their value is unobservable by definition!

My #EconJMP tackles this problem 1/

![Robust Estimation of Private Business Wealth*

Job Market Paper

Simon J. Toussaint†

November 14, 2024

[Most recent version here]

Abstract

Estimating the market value of private businesses is essential for understanding both aggregate firm dynamics and top wealth

inequality, yet these values are inherently unobservable. This paper introduces an econometric approach that treats the gap

between true market values and initial estimates as measurement error. I employ time-series restrictions on these errors as

moment conditions within a GMM framework, and use the fitted values from these estimations as error-free estimates of

private business wealth and capital stocks. Applying this method to Dutch administrative data linking the universe of firms

to their owners, I find that aggregate private business wealth increases by 30% of GDP initially, and is more stable than the

unadjusted series. Top 1% and 0.1% wealth shares increase by 3–5 percentage points, peaking at 38% and 20%, respectively.

Adjusted returns to firm wealth exhibit a steeper gradient across the wealth distribution than unadjusted returns, consistent

with models of return heterogeneity.](https://cdn.bsky.app/img/feed_thumbnail/plain/did:plc:wus4g34bpbzjefp547irpkeu/bafkreibg34g2k7zwmjqytkllrcxfsj5tnov22hdny74qz7ks5jwa5csbou@jpeg)

November 14, 2024 at 5:17 PM

📯 Job Market Paper Alert 📯

Private businesses make up 50% of sales & profits and are the main wealth component of the wealthiest households. So, what is their value? Well, that's difficult, since they're not listed: their value is unobservable by definition!

My #EconJMP tackles this problem 1/

Private businesses make up 50% of sales & profits and are the main wealth component of the wealthiest households. So, what is their value? Well, that's difficult, since they're not listed: their value is unobservable by definition!

My #EconJMP tackles this problem 1/

Reposted by Arthur Apostel

Final week to register for our workshop "The Paradox of Belgian Inequality" on Dec 3.

In this workshop, we present the results of a 4-year research project funded by BELSPO and carried out by the KU Leuven, the University of Antwerp and the ULB.

Registration via: feb.kuleuven.be/drc/Economic...

In this workshop, we present the results of a 4-year research project funded by BELSPO and carried out by the KU Leuven, the University of Antwerp and the ULB.

Registration via: feb.kuleuven.be/drc/Economic...

November 19, 2024 at 9:42 AM

Final week to register for our workshop "The Paradox of Belgian Inequality" on Dec 3.

In this workshop, we present the results of a 4-year research project funded by BELSPO and carried out by the KU Leuven, the University of Antwerp and the ULB.

Registration via: feb.kuleuven.be/drc/Economic...

In this workshop, we present the results of a 4-year research project funded by BELSPO and carried out by the KU Leuven, the University of Antwerp and the ULB.

Registration via: feb.kuleuven.be/drc/Economic...