Felix Geiger

@flxgeiger.bsky.social

@bundesbank | views are my own | private | monetary policy, financial markets, finance, economics | retweets, likes and following do not imply endorsement

𝗡𝗲𝘄 𝗥𝗲𝘀𝗲𝗮𝗿𝗰𝗵: 𝗠𝗜𝗟𝗔 (𝗠𝗼𝗻𝗲𝘁𝗮𝗿𝘆-𝗜𝗻𝘁𝗲𝗹𝗹𝗶𝗴𝗲𝗻𝘁 𝗟𝗮𝗻𝗴𝘂𝗮𝗴𝗲 𝗔𝗴𝗲𝗻𝘁)

We introduce MILA—a new AI-driven solution for analyzing central bank communication.

MILA operates on individual sentences by using the macro and in-document context. 1/n

We introduce MILA—a new AI-driven solution for analyzing central bank communication.

MILA operates on individual sentences by using the macro and in-document context. 1/n

April 9, 2025 at 9:22 PM

𝗡𝗲𝘄 𝗥𝗲𝘀𝗲𝗮𝗿𝗰𝗵: 𝗠𝗜𝗟𝗔 (𝗠𝗼𝗻𝗲𝘁𝗮𝗿𝘆-𝗜𝗻𝘁𝗲𝗹𝗹𝗶𝗴𝗲𝗻𝘁 𝗟𝗮𝗻𝗴𝘂𝗮𝗴𝗲 𝗔𝗴𝗲𝗻𝘁)

We introduce MILA—a new AI-driven solution for analyzing central bank communication.

MILA operates on individual sentences by using the macro and in-document context. 1/n

We introduce MILA—a new AI-driven solution for analyzing central bank communication.

MILA operates on individual sentences by using the macro and in-document context. 1/n

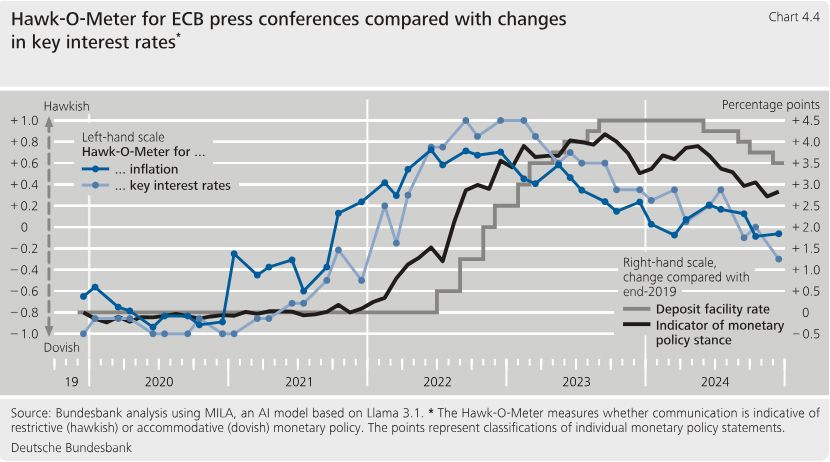

How to measure the broader monetary policy stance in the euro area?

In our latest @bundesbank.de report, we present the proxy monetary policy rate, which combines information from the risk-free yield curve and risk assets. 1\ #EconSky @plieberk.bsky.social

In our latest @bundesbank.de report, we present the proxy monetary policy rate, which combines information from the risk-free yield curve and risk assets. 1\ #EconSky @plieberk.bsky.social

March 20, 2025 at 1:36 PM

How to measure the broader monetary policy stance in the euro area?

In our latest @bundesbank.de report, we present the proxy monetary policy rate, which combines information from the risk-free yield curve and risk assets. 1\ #EconSky @plieberk.bsky.social

In our latest @bundesbank.de report, we present the proxy monetary policy rate, which combines information from the risk-free yield curve and risk assets. 1\ #EconSky @plieberk.bsky.social

Since 2011, the tone of the ECB Executive Board’s monetary policy speeches has evolved in line with the ECB press conferences and the macroeconomic environment in the euro area. Some dispersion of speeches visible during the recent tightening and easing phase. \4

March 18, 2025 at 8:55 PM

Since 2011, the tone of the ECB Executive Board’s monetary policy speeches has evolved in line with the ECB press conferences and the macroeconomic environment in the euro area. Some dispersion of speeches visible during the recent tightening and easing phase. \4

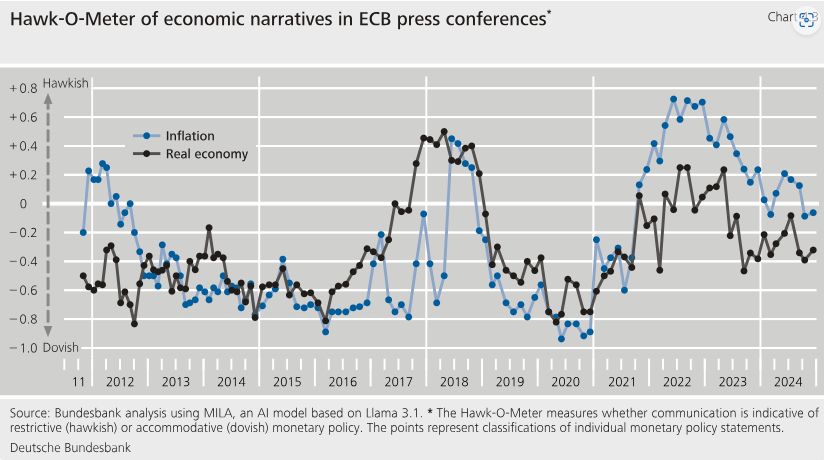

𝗦𝗵𝗶𝗳𝘁𝗶𝗻𝗴 𝗽𝗼𝗹𝗶𝗰𝘆 𝘀𝗶𝗴𝗻𝗮𝗹𝘀: MILA detects a dovish stance in 2020; a balanced inflation narrative in 2021, but still a dovish rate outlook; then a hawkish shift in 2022-23. By 2024, communication became more balanced. \3

March 18, 2025 at 8:55 PM

𝗦𝗵𝗶𝗳𝘁𝗶𝗻𝗴 𝗽𝗼𝗹𝗶𝗰𝘆 𝘀𝗶𝗴𝗻𝗮𝗹𝘀: MILA detects a dovish stance in 2020; a balanced inflation narrative in 2021, but still a dovish rate outlook; then a hawkish shift in 2022-23. By 2024, communication became more balanced. \3

𝗔𝗜-𝗽𝗼𝘄𝗲𝗿𝗲𝗱 𝗮𝗻𝗮𝗹𝘆𝘀𝗶𝘀: MILA provides structured assessments of ECB communication from 2011 to 2024, analyzing around 50,000 sentences on an individual basis. \2

March 18, 2025 at 8:55 PM

𝗔𝗜-𝗽𝗼𝘄𝗲𝗿𝗲𝗱 𝗮𝗻𝗮𝗹𝘆𝘀𝗶𝘀: MILA provides structured assessments of ECB communication from 2011 to 2024, analyzing around 50,000 sentences on an individual basis. \2

At @bundesbank.de, we have developed 𝗠𝗜𝗟𝗔 (𝗠𝗼𝗻𝗲𝘁𝗮𝗿𝘆-𝗜𝗻𝘁𝗲𝗹𝗹𝗶𝗴𝗲𝗻𝘁 𝗟𝗮𝗻𝗴𝘂𝗮𝗴𝗲 𝗔𝗴𝗲𝗻𝘁) - an AI tool designed to evaluate ECB communication, assessing individual sentences from monetary policy statements and speeches given in-document as well as the macro context. \1 #EconSky

March 18, 2025 at 8:55 PM

At @bundesbank.de, we have developed 𝗠𝗜𝗟𝗔 (𝗠𝗼𝗻𝗲𝘁𝗮𝗿𝘆-𝗜𝗻𝘁𝗲𝗹𝗹𝗶𝗴𝗲𝗻𝘁 𝗟𝗮𝗻𝗴𝘂𝗮𝗴𝗲 𝗔𝗴𝗲𝗻𝘁) - an AI tool designed to evaluate ECB communication, assessing individual sentences from monetary policy statements and speeches given in-document as well as the macro context. \1 #EconSky

The script has flipped 🌎

- Euro area macro drives euro yields aka Bunds up

- US macro drives these yields down.

- Euro area macro drives euro yields aka Bunds up

- US macro drives these yields down.

March 6, 2025 at 5:41 PM

The script has flipped 🌎

- Euro area macro drives euro yields aka Bunds up

- US macro drives these yields down.

- Euro area macro drives euro yields aka Bunds up

- US macro drives these yields down.

US Treasuries: slide. 🛝

Bunds: hold my beer. 🍺

Bunds: hold my beer. 🍺

March 6, 2025 at 12:41 PM

US Treasuries: slide. 🛝

Bunds: hold my beer. 🍺

Bunds: hold my beer. 🍺

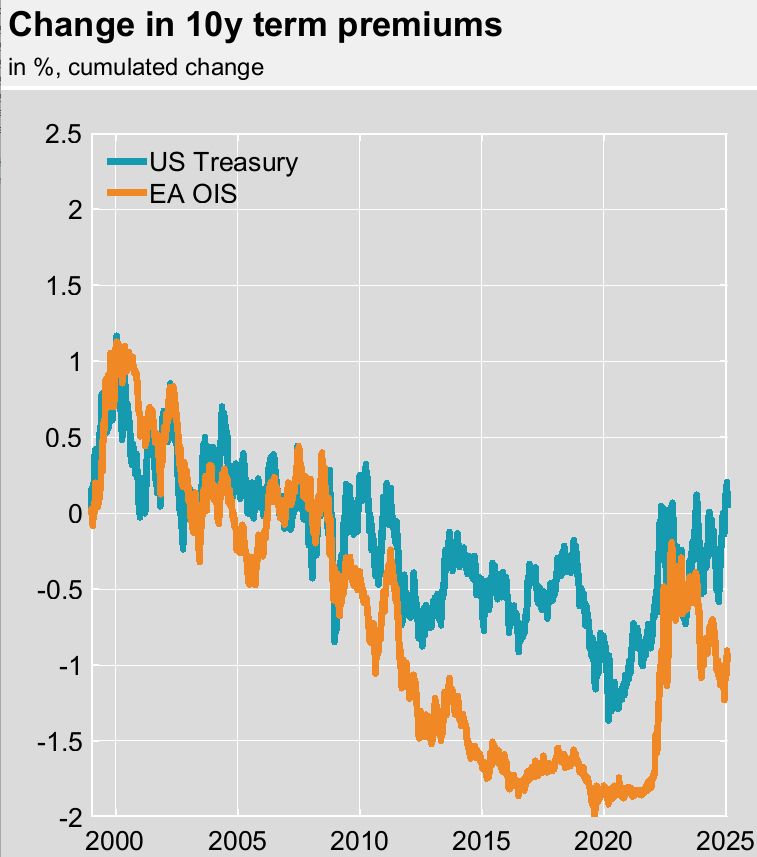

Still, there are signficant level differences between US and EA yield curve components. 3/n

January 31, 2025 at 1:20 PM

Still, there are signficant level differences between US and EA yield curve components. 3/n

Corresponding change in average short-term rate expectations shows close co-movement since 1999 with EA expectations typically lagging its US peers (if at all). 2/n

January 31, 2025 at 1:20 PM

Corresponding change in average short-term rate expectations shows close co-movement since 1999 with EA expectations typically lagging its US peers (if at all). 2/n

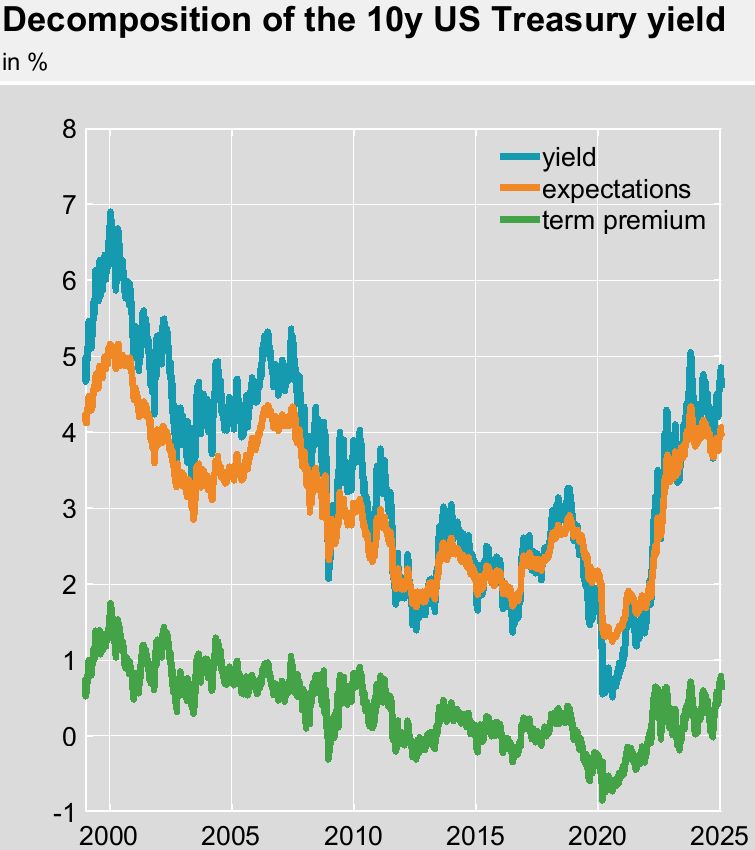

🧵As 𝘁𝗲𝗿𝗺 𝗽𝗿𝗲𝗺𝗶𝘂𝗺𝘀 took center stage these days - Chart depicts dynamics for US and EA 1/n

➡️99-12: strong co-movement

➡️12-20: EA term premium collapses relative to US

➡️22-24: de-compression more pronounced in EA

➡️since mid-24: degree of US term premium rise is only partly matched by EA

#EconSky

➡️99-12: strong co-movement

➡️12-20: EA term premium collapses relative to US

➡️22-24: de-compression more pronounced in EA

➡️since mid-24: degree of US term premium rise is only partly matched by EA

#EconSky

January 31, 2025 at 1:20 PM

🧵As 𝘁𝗲𝗿𝗺 𝗽𝗿𝗲𝗺𝗶𝘂𝗺𝘀 took center stage these days - Chart depicts dynamics for US and EA 1/n

➡️99-12: strong co-movement

➡️12-20: EA term premium collapses relative to US

➡️22-24: de-compression more pronounced in EA

➡️since mid-24: degree of US term premium rise is only partly matched by EA

#EconSky

➡️99-12: strong co-movement

➡️12-20: EA term premium collapses relative to US

➡️22-24: de-compression more pronounced in EA

➡️since mid-24: degree of US term premium rise is only partly matched by EA

#EconSky

The 𝗿𝗶𝘀𝗸 𝗮𝗽𝗽𝗲𝘁𝗶𝘁𝗲 𝗰𝗵𝗮𝗻𝗻𝗲𝗹 amplifies monetary policy’s impact on inflation and GDP. Without it, transmission is notably weaker. 4/n

January 21, 2025 at 1:42 PM

The 𝗿𝗶𝘀𝗸 𝗮𝗽𝗽𝗲𝘁𝗶𝘁𝗲 𝗰𝗵𝗮𝗻𝗻𝗲𝗹 amplifies monetary policy’s impact on inflation and GDP. Without it, transmission is notably weaker. 4/n

𝗠𝗼𝗻𝗲𝘁𝗮𝗿𝘆 𝗽𝗼𝗹𝗶𝗰𝘆 in the euro area and the US significantly influences risk sentiment, with diverse exchange rate effects. 3/n

January 21, 2025 at 1:42 PM

𝗠𝗼𝗻𝗲𝘁𝗮𝗿𝘆 𝗽𝗼𝗹𝗶𝗰𝘆 in the euro area and the US significantly influences risk sentiment, with diverse exchange rate effects. 3/n

𝗧𝗶𝗺𝗲-𝘃𝗮𝗿𝘆𝗶𝗻𝗴 𝗿𝗶𝘀𝗸 𝗮𝗽𝗽𝗲𝘁𝗶𝘁𝗲 amplifies risk premiums, especially during crises. This is a robust feature across various indicators including the work by @michaeldbauer.bsky.social and Carolin Pflueger (et al). 2/n

January 21, 2025 at 1:42 PM

𝗧𝗶𝗺𝗲-𝘃𝗮𝗿𝘆𝗶𝗻𝗴 𝗿𝗶𝘀𝗸 𝗮𝗽𝗽𝗲𝘁𝗶𝘁𝗲 amplifies risk premiums, especially during crises. This is a robust feature across various indicators including the work by @michaeldbauer.bsky.social and Carolin Pflueger (et al). 2/n

🧵In our latest report of @bundesbank.de, we examine how 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀' 𝗿𝗶𝘀𝗸 𝗮𝗽𝗽𝗲𝘁𝗶𝘁𝗲 in the euro area interacts with 𝗺𝗼𝗻𝗲𝘁𝗮𝗿𝘆 𝗽𝗼𝗹𝗶𝗰𝘆 𝘁𝗼 𝘀𝗵𝗮𝗽𝗲 𝗺𝗮𝗰𝗿𝗼𝗲𝗰𝗼𝗻𝗼𝗺𝗶𝗰 𝗼𝘂𝘁𝗰𝗼𝗺𝗲𝘀. Key takeaways ⬇️1/n #EconSky

January 21, 2025 at 1:42 PM

🧵In our latest report of @bundesbank.de, we examine how 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀' 𝗿𝗶𝘀𝗸 𝗮𝗽𝗽𝗲𝘁𝗶𝘁𝗲 in the euro area interacts with 𝗺𝗼𝗻𝗲𝘁𝗮𝗿𝘆 𝗽𝗼𝗹𝗶𝗰𝘆 𝘁𝗼 𝘀𝗵𝗮𝗽𝗲 𝗺𝗮𝗰𝗿𝗼𝗲𝗰𝗼𝗻𝗼𝗺𝗶𝗰 𝗼𝘂𝘁𝗰𝗼𝗺𝗲𝘀. Key takeaways ⬇️1/n #EconSky

Great paper showing why the US economy keeps surprising to the upside despite high policy rates.

➡️Financial conditions may be loose with high stock valuations and compressed risk spreads

➡️For the economy these conditions matter

➡️By targeting financial conditions, Fed may reduce output volatility

➡️Financial conditions may be loose with high stock valuations and compressed risk spreads

➡️For the economy these conditions matter

➡️By targeting financial conditions, Fed may reduce output volatility

January 16, 2025 at 3:05 PM

Great paper showing why the US economy keeps surprising to the upside despite high policy rates.

➡️Financial conditions may be loose with high stock valuations and compressed risk spreads

➡️For the economy these conditions matter

➡️By targeting financial conditions, Fed may reduce output volatility

➡️Financial conditions may be loose with high stock valuations and compressed risk spreads

➡️For the economy these conditions matter

➡️By targeting financial conditions, Fed may reduce output volatility

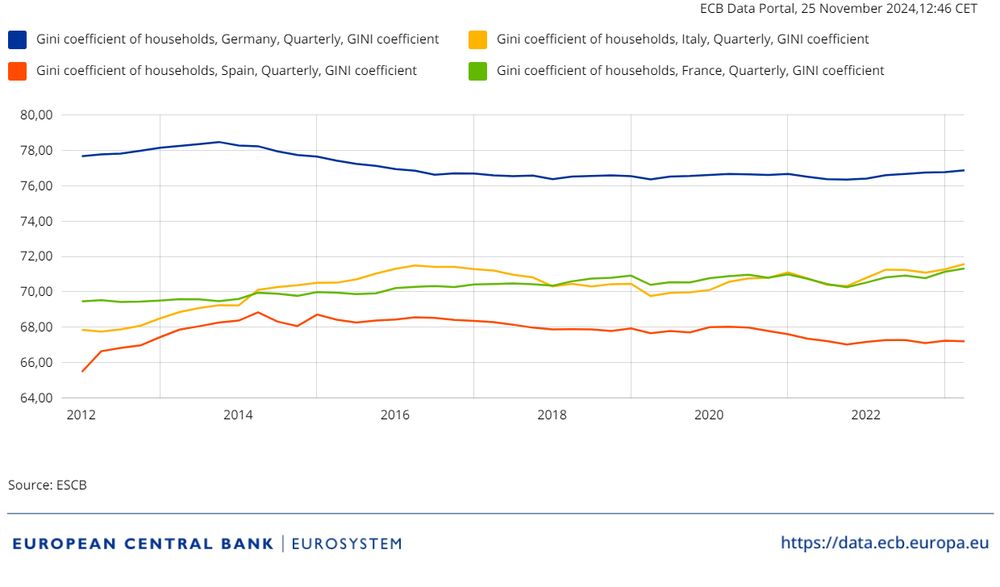

here: Gini coefficient of households at the country level 2/3

November 25, 2024 at 11:53 AM

here: Gini coefficient of households at the country level 2/3

Distributional Wealth Accounts in the Euro Area

➡️still impressed by this quite new and highly valuable quarterly data set

➡️still impressed by the evolution of key metrics

here: median net wealth at the country level 1/3

➡️still impressed by this quite new and highly valuable quarterly data set

➡️still impressed by the evolution of key metrics

here: median net wealth at the country level 1/3

November 25, 2024 at 11:53 AM

Distributional Wealth Accounts in the Euro Area

➡️still impressed by this quite new and highly valuable quarterly data set

➡️still impressed by the evolution of key metrics

here: median net wealth at the country level 1/3

➡️still impressed by this quite new and highly valuable quarterly data set

➡️still impressed by the evolution of key metrics

here: median net wealth at the country level 1/3

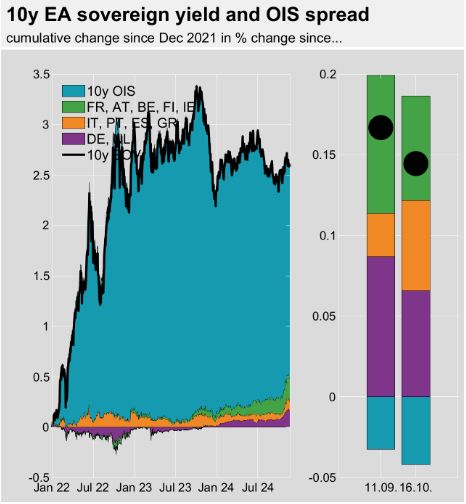

With Bunds loosening their "specialness", EA sovereign spreads compressed only against Bunds, not against the risk-free OIS rate. Quite interesting that EA sovereign yields likeswise selled-off (to a lower extent than Bunds), while the OIS rate essentially fell recently.

bsky.app/profile/flxg...

bsky.app/profile/flxg...

November 24, 2024 at 9:21 AM

With Bunds loosening their "specialness", EA sovereign spreads compressed only against Bunds, not against the risk-free OIS rate. Quite interesting that EA sovereign yields likeswise selled-off (to a lower extent than Bunds), while the OIS rate essentially fell recently.

bsky.app/profile/flxg...

bsky.app/profile/flxg...

Corporate insolvencies in Germany have risen further in 2024, but from low levels.

Source: publikationen.bundesbank.de/publikatione...

Source: publikationen.bundesbank.de/publikatione...

November 21, 2024 at 10:12 PM

Corporate insolvencies in Germany have risen further in 2024, but from low levels.

Source: publikationen.bundesbank.de/publikatione...

Source: publikationen.bundesbank.de/publikatione...

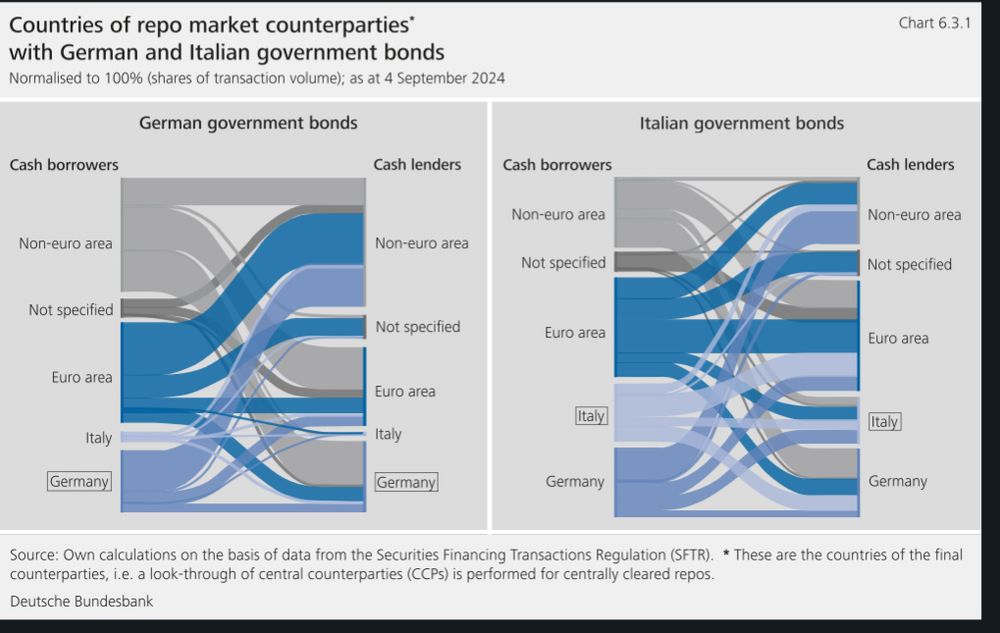

Most repos secured by Italian government bonds are traded between counterparties within the euro area, particularly counterparties from Germany.

By contrast, repos with German government bonds often involve counterparties outside the euro area.

Source: publikationen.bundesbank.de/publikatione...

By contrast, repos with German government bonds often involve counterparties outside the euro area.

Source: publikationen.bundesbank.de/publikatione...

November 21, 2024 at 10:04 PM

Most repos secured by Italian government bonds are traded between counterparties within the euro area, particularly counterparties from Germany.

By contrast, repos with German government bonds often involve counterparties outside the euro area.

Source: publikationen.bundesbank.de/publikatione...

By contrast, repos with German government bonds often involve counterparties outside the euro area.

Source: publikationen.bundesbank.de/publikatione...

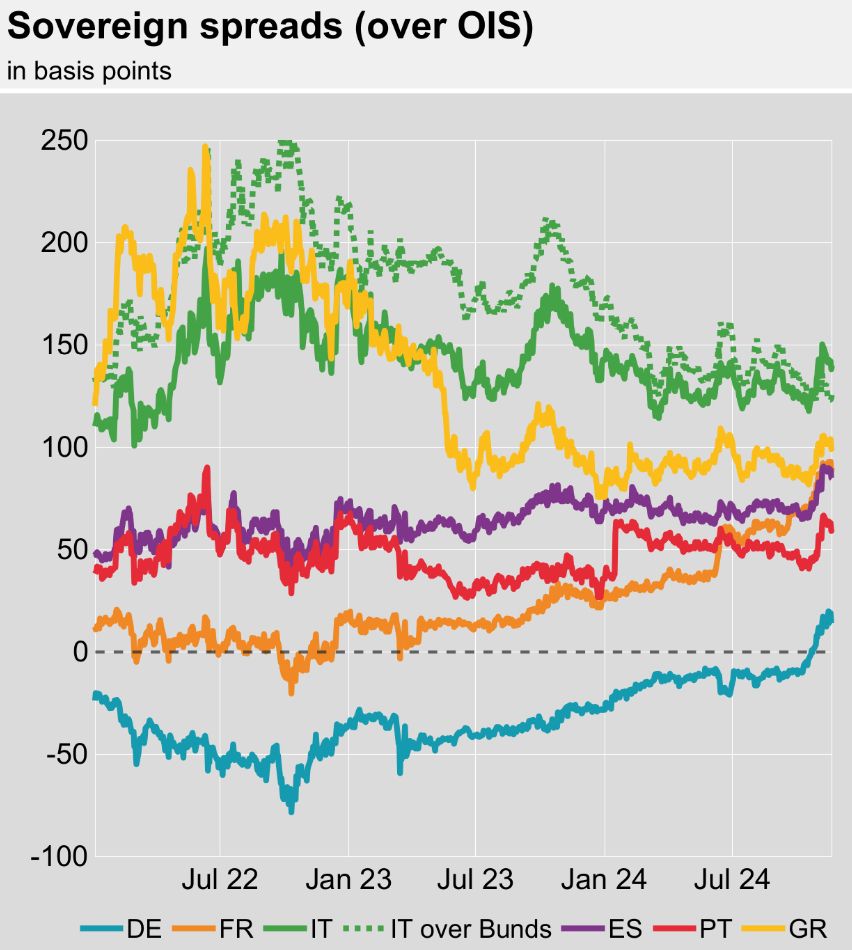

➡️ 𝗙𝗿𝗲𝗻𝗰𝗵 𝘀𝗽𝗿𝗲𝗮𝗱𝘀 over risk-free OIS rates will likely to remain in this chart when monitoring EA spreads.

➡️Italian spread over Bunds trading lower than over OIS. This reflects regime change with 𝗕𝘂𝗻𝗱𝘀 𝘀𝗲𝗹𝗹𝗶𝗻𝗴 𝗼𝗳𝗳 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝗢𝗜𝗦 recently.

2 𝗶𝗺𝗽𝗼𝗿𝘁𝗮𝗻𝘁 𝘀𝗵𝗶𝗳𝘁𝘀 𝗶𝗻 𝗘𝗔 𝘀𝗼𝘃𝗲𝗿𝗲𝗶𝗴𝗻 𝘀𝗽𝗿𝗲𝗮𝗱 𝗱𝗿𝗶𝘃𝗲𝗿𝘀.

#Econsky

➡️Italian spread over Bunds trading lower than over OIS. This reflects regime change with 𝗕𝘂𝗻𝗱𝘀 𝘀𝗲𝗹𝗹𝗶𝗻𝗴 𝗼𝗳𝗳 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝗢𝗜𝗦 recently.

2 𝗶𝗺𝗽𝗼𝗿𝘁𝗮𝗻𝘁 𝘀𝗵𝗶𝗳𝘁𝘀 𝗶𝗻 𝗘𝗔 𝘀𝗼𝘃𝗲𝗿𝗲𝗶𝗴𝗻 𝘀𝗽𝗿𝗲𝗮𝗱 𝗱𝗿𝗶𝘃𝗲𝗿𝘀.

#Econsky

November 21, 2024 at 5:13 PM

➡️ 𝗙𝗿𝗲𝗻𝗰𝗵 𝘀𝗽𝗿𝗲𝗮𝗱𝘀 over risk-free OIS rates will likely to remain in this chart when monitoring EA spreads.

➡️Italian spread over Bunds trading lower than over OIS. This reflects regime change with 𝗕𝘂𝗻𝗱𝘀 𝘀𝗲𝗹𝗹𝗶𝗻𝗴 𝗼𝗳𝗳 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝗢𝗜𝗦 recently.

2 𝗶𝗺𝗽𝗼𝗿𝘁𝗮𝗻𝘁 𝘀𝗵𝗶𝗳𝘁𝘀 𝗶𝗻 𝗘𝗔 𝘀𝗼𝘃𝗲𝗿𝗲𝗶𝗴𝗻 𝘀𝗽𝗿𝗲𝗮𝗱 𝗱𝗿𝗶𝘃𝗲𝗿𝘀.

#Econsky

➡️Italian spread over Bunds trading lower than over OIS. This reflects regime change with 𝗕𝘂𝗻𝗱𝘀 𝘀𝗲𝗹𝗹𝗶𝗻𝗴 𝗼𝗳𝗳 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝗢𝗜𝗦 recently.

2 𝗶𝗺𝗽𝗼𝗿𝘁𝗮𝗻𝘁 𝘀𝗵𝗶𝗳𝘁𝘀 𝗶𝗻 𝗘𝗔 𝘀𝗼𝘃𝗲𝗿𝗲𝗶𝗴𝗻 𝘀𝗽𝗿𝗲𝗮𝗱 𝗱𝗿𝗶𝘃𝗲𝗿𝘀.

#Econsky

Market-based inflation indicators declined slightly over the period under review. 𝗙𝗼𝗿 2025, 𝗺𝗮𝗿𝗸𝗲𝘁-𝗯𝗮𝘀𝗲𝗱 𝗶𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝗲𝘅𝗽𝗲𝗰𝘁𝗮𝘁𝗶𝗼𝗻𝘀 𝗰𝗮𝗹𝗰𝘂𝗹𝗮𝘁𝗲𝗱 𝗼𝗻 𝘁𝗵𝗲 𝗯𝗮𝘀𝗶𝘀 𝗼𝗳 𝗲𝘂𝗿𝗼 𝗮𝗿𝗲𝗮 𝗶𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝘀𝘄𝗮𝗽𝘀 𝘀𝘁𝗮𝗻𝗱 𝗮𝗿𝗼𝘂𝗻𝗱 2%. Most recently market and survey data have shown significant convergence. 5/6

November 21, 2024 at 11:05 AM

Market-based inflation indicators declined slightly over the period under review. 𝗙𝗼𝗿 2025, 𝗺𝗮𝗿𝗸𝗲𝘁-𝗯𝗮𝘀𝗲𝗱 𝗶𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝗲𝘅𝗽𝗲𝗰𝘁𝗮𝘁𝗶𝗼𝗻𝘀 𝗰𝗮𝗹𝗰𝘂𝗹𝗮𝘁𝗲𝗱 𝗼𝗻 𝘁𝗵𝗲 𝗯𝗮𝘀𝗶𝘀 𝗼𝗳 𝗲𝘂𝗿𝗼 𝗮𝗿𝗲𝗮 𝗶𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝘀𝘄𝗮𝗽𝘀 𝘀𝘁𝗮𝗻𝗱 𝗮𝗿𝗼𝘂𝗻𝗱 2%. Most recently market and survey data have shown significant convergence. 5/6