Recently published in

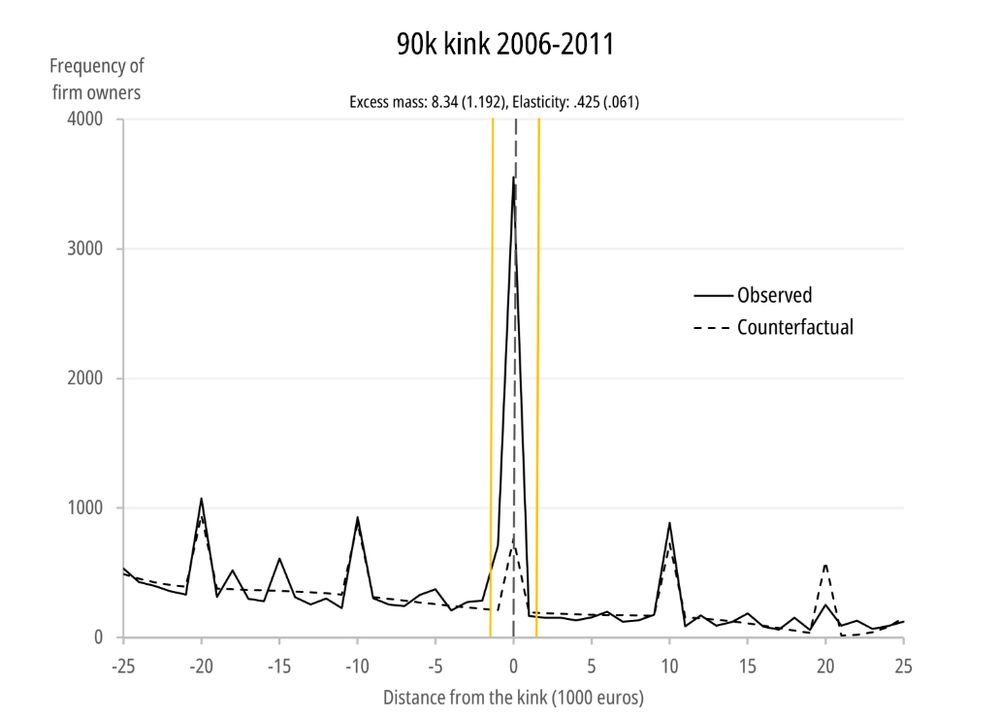

@itaxjournal.bsky.social "Taxpayer response to greater progressivity: evidence from personal income tax reform in Uganda" by Maria Jouste, Tina Kaidu Barugahara, Joseph Ayo Okello, Jukka Pirttilä & Pia Rattenhuber

Available at:

rdcu.be/eI3rM