Jim Paulsen

@jimwpaulsen.bsky.social

PhD economist by training. 40 years as a Chief Investment Strategist still following the economy & financial markets at http://paulsenperspectives.Substack.com

The Fed funds rate has been trailing real commodity prices by about two years since 2020. Should Fed policy remain "lagged & tardy", commodity prices suggest a 2.25%ish funds rate and a 3%ish 10-year yield by the end of 2026. See my latest free report @ paulsenperspectives.substack.com

December 24, 2025 at 1:03 PM

The Fed funds rate has been trailing real commodity prices by about two years since 2020. Should Fed policy remain "lagged & tardy", commodity prices suggest a 2.25%ish funds rate and a 3%ish 10-year yield by the end of 2026. See my latest free report @ paulsenperspectives.substack.com

The SP 500 PE ratio has been high throughout this bull market, but Main Street confidence remains pessimistic, and the stock market keeps climbing. Maybe a better valuation guide is the Emotion-Adjusted PE. For all the details, see my latest report at paulsenperspectives.substack.com

December 22, 2025 at 12:44 PM

The SP 500 PE ratio has been high throughout this bull market, but Main Street confidence remains pessimistic, and the stock market keeps climbing. Maybe a better valuation guide is the Emotion-Adjusted PE. For all the details, see my latest report at paulsenperspectives.substack.com

Investors often don't realize that changes in Main Street confidence are just as impactful as changes in EPS. I suspect 2026 will be primarily driven by a confidence revival even if EPS flatten. See my latest for all the details @ paulsenperspectives.substack.com

December 18, 2025 at 4:09 PM

Investors often don't realize that changes in Main Street confidence are just as impactful as changes in EPS. I suspect 2026 will be primarily driven by a confidence revival even if EPS flatten. See my latest for all the details @ paulsenperspectives.substack.com

Despite the federal debt to GDP ratio rising steadily during the last 40 years, the 10-year Tbond yield has persistently declined! Bond Vigilante sightings appear to be more folklore than fact! See my latest report @ paulsenperspectives.substack.com

December 15, 2025 at 12:58 PM

Despite the federal debt to GDP ratio rising steadily during the last 40 years, the 10-year Tbond yield has persistently declined! Bond Vigilante sightings appear to be more folklore than fact! See my latest report @ paulsenperspectives.substack.com

Despite all the hand wringing over inflation, recession and tariffs, the US economy has mostly been in the sweet spot for equity investors in recent years -- not too hot nor too cold. Maybe investors should just chill until the economy leaves the "sweet spot"? PaulsenPerspectives.Substack.com

December 11, 2025 at 1:02 PM

Despite all the hand wringing over inflation, recession and tariffs, the US economy has mostly been in the sweet spot for equity investors in recent years -- not too hot nor too cold. Maybe investors should just chill until the economy leaves the "sweet spot"? PaulsenPerspectives.Substack.com

During the govt. shutdown, economic data was delayed, but the relative performance of cyclical stocks continued to provide a daily read on overall economic momentum. The real-time performance of cyclicals continues to suggest US economic conditions remain punk. PaulsenPerspectives.Substack.com

December 10, 2025 at 6:08 PM

During the govt. shutdown, economic data was delayed, but the relative performance of cyclical stocks continued to provide a daily read on overall economic momentum. The real-time performance of cyclicals continues to suggest US economic conditions remain punk. PaulsenPerspectives.Substack.com

The Copper/Gold Price has been steadily declining since mid-2022 -- when CPI Inflation Peaked -- and continues to suggest the Fed Funds Rate is WAY too high. Dr. Copper is indicating the Fed may be cutting rates many more times as we enter 2026. paulsenperspectives.substack.com

December 9, 2025 at 2:21 PM

The Copper/Gold Price has been steadily declining since mid-2022 -- when CPI Inflation Peaked -- and continues to suggest the Fed Funds Rate is WAY too high. Dr. Copper is indicating the Fed may be cutting rates many more times as we enter 2026. paulsenperspectives.substack.com

Economic growth has slowed to unacceptable levels, says author Jim Paulsen cnb.cx/4iE39CF

I had the great pleasure joining @jonfortt on @CNBCOvertime

yesterday. Hope you enjoy the discussion. Thanks for having me, Jon!

paulsenperspectives.substack.com

I had the great pleasure joining @jonfortt on @CNBCOvertime

yesterday. Hope you enjoy the discussion. Thanks for having me, Jon!

paulsenperspectives.substack.com

Economic growth has slowed to unacceptable levels, says author Jim Paulsen

Jim Paulsen, Paulsen Perspectives author, and Charles Bobrinskoy, Ariel Investments vice chairman, joins 'Closing Bell Overtime' to talk the day's market action and the state of the U.S. economy.

cnb.cx

December 5, 2025 at 12:49 PM

Economic growth has slowed to unacceptable levels, says author Jim Paulsen cnb.cx/4iE39CF

I had the great pleasure joining @jonfortt on @CNBCOvertime

yesterday. Hope you enjoy the discussion. Thanks for having me, Jon!

paulsenperspectives.substack.com

I had the great pleasure joining @jonfortt on @CNBCOvertime

yesterday. Hope you enjoy the discussion. Thanks for having me, Jon!

paulsenperspectives.substack.com

My latest missive "Stock Market Signaling Economic Weakness" notes several key equity metrics pointing to weaker real US growth than widely perceived which should force persistent Fed easing well into 2026. A couple examples are show below. See full report at:

paulsenperspectives.substack.com

paulsenperspectives.substack.com

December 4, 2025 at 1:48 PM

My latest missive "Stock Market Signaling Economic Weakness" notes several key equity metrics pointing to weaker real US growth than widely perceived which should force persistent Fed easing well into 2026. A couple examples are show below. See full report at:

paulsenperspectives.substack.com

paulsenperspectives.substack.com

Monday, I had the great pleasure of again joining

@practicalquant and @jjcarbonneau from the Excess Return Podcast for a fourth monthly edition. Thanks for taking a watch & listen. paulsenperspectives.substack.com

www.youtube.com/watch?v=a030...

@practicalquant and @jjcarbonneau from the Excess Return Podcast for a fourth monthly edition. Thanks for taking a watch & listen. paulsenperspectives.substack.com

www.youtube.com/watch?v=a030...

The Fed Is Fighting the Wrong War | Jim Paulsen on Why 3% Inflation Isn't the Problem

YouTube video by Excess Returns

www.youtube.com

December 2, 2025 at 5:35 PM

Monday, I had the great pleasure of again joining

@practicalquant and @jjcarbonneau from the Excess Return Podcast for a fourth monthly edition. Thanks for taking a watch & listen. paulsenperspectives.substack.com

www.youtube.com/watch?v=a030...

@practicalquant and @jjcarbonneau from the Excess Return Podcast for a fourth monthly edition. Thanks for taking a watch & listen. paulsenperspectives.substack.com

www.youtube.com/watch?v=a030...

See my latest report on cyclical stocks outperforming, technology stocks' monetary policy invariance, jobless claims failure, stock-bond correlation & Fed easing, bond yields to head toward 3%, the power of cash & tech runs, and more @ paulsenperspectives.substack.com

December 1, 2025 at 12:33 PM

See my latest report on cyclical stocks outperforming, technology stocks' monetary policy invariance, jobless claims failure, stock-bond correlation & Fed easing, bond yields to head toward 3%, the power of cash & tech runs, and more @ paulsenperspectives.substack.com

As economic policy stimulus (TPS) expands, expect stock market leadership to shift from innovative new era stocks to "policy-pushed" old era stocks. For all the details, see my latest piece at: paulsenperspectives.substack.com

November 24, 2025 at 1:01 PM

As economic policy stimulus (TPS) expands, expect stock market leadership to shift from innovative new era stocks to "policy-pushed" old era stocks. For all the details, see my latest piece at: paulsenperspectives.substack.com

Earlier this week, I had the great privilege of joining the Wealth Consulting Group on their regular podcast. Jim, Talley and Paisley are pros and great to work with. We covered a lot of diverse issues. Thanks for having me!

PaulsenPerspectives.Substack.com

youtu.be/9XecRL_QNvc

PaulsenPerspectives.Substack.com

youtu.be/9XecRL_QNvc

The Bull of Wall Street #49 – 'Paulsen Perspectives' author Jim Paulsen (recorded 11/17/25)

YouTube video by The Wealth Consulting Group

youtu.be

November 21, 2025 at 3:01 PM

Earlier this week, I had the great privilege of joining the Wealth Consulting Group on their regular podcast. Jim, Talley and Paisley are pros and great to work with. We covered a lot of diverse issues. Thanks for having me!

PaulsenPerspectives.Substack.com

youtu.be/9XecRL_QNvc

PaulsenPerspectives.Substack.com

youtu.be/9XecRL_QNvc

Job numbers are punk, and the unemployment rate is up to 4.4%. Trends in public company employment are even worse. Policy officials need to make job creation "the" priority! Check out my work at paulsenperspectives.substack.com

November 20, 2025 at 6:43 PM

Job numbers are punk, and the unemployment rate is up to 4.4%. Trends in public company employment are even worse. Policy officials need to make job creation "the" priority! Check out my work at paulsenperspectives.substack.com

US Inflation has been calm for the past 3 years. Real GDP growth & jobs have been subpar for 20 years and both are currently punk. Why do policy officials continue to emphasize fighting inflation rather than promoting/supporting real growth? See my latest report @ paulsenperspectives.substack.com

November 20, 2025 at 1:11 PM

US Inflation has been calm for the past 3 years. Real GDP growth & jobs have been subpar for 20 years and both are currently punk. Why do policy officials continue to emphasize fighting inflation rather than promoting/supporting real growth? See my latest report @ paulsenperspectives.substack.com

The Main Street Meter has a strong inverse relationship with future stock market returns. It has declined substantially suggesting the stock market is "younger" and more attractive than 22% of time since 1955! See my latest report for all the details at: paulsenperspectives.substack.com

November 17, 2025 at 12:36 PM

The Main Street Meter has a strong inverse relationship with future stock market returns. It has declined substantially suggesting the stock market is "younger" and more attractive than 22% of time since 1955! See my latest report for all the details at: paulsenperspectives.substack.com

I had the pleasure of joining Morgan Brennan & Jon Fortt on CNBC Overtime Friday. We had a lively discussion about the stock market, broader market plays, and the tech bubble. Thanks to both Morgan & Jon for having me. Have a listen!

PaulsenPerspectives.Substack.com

www.youtube.com/watch?v=av4_...

PaulsenPerspectives.Substack.com

www.youtube.com/watch?v=av4_...

LinkedIn

This link will take you to a page that’s not on LinkedIn

lnkd.in

November 10, 2025 at 12:44 PM

I had the pleasure of joining Morgan Brennan & Jon Fortt on CNBC Overtime Friday. We had a lively discussion about the stock market, broader market plays, and the tech bubble. Thanks to both Morgan & Jon for having me. Have a listen!

PaulsenPerspectives.Substack.com

www.youtube.com/watch?v=av4_...

PaulsenPerspectives.Substack.com

www.youtube.com/watch?v=av4_...

The Stock Market is entering its historically strongest part of the year (November through April) after performance during its weakest part (May thru Oct) was STRONG. Both seasonal results point to additional solid stock market returns. See my full report for free @ paulsenperspectives.substack.com

October 30, 2025 at 11:59 AM

The Stock Market is entering its historically strongest part of the year (November through April) after performance during its weakest part (May thru Oct) was STRONG. Both seasonal results point to additional solid stock market returns. See my full report for free @ paulsenperspectives.substack.com

Participation in this bull market has been extremely narrow. However, for the 1st time in about 2 years, RTY's EPS is outpacing S&P EPS. Maybe more accommodative economic policies are starting to awaken broader parts of the stock market? paulsenperspectives.subtack.com

October 28, 2025 at 7:28 PM

Participation in this bull market has been extremely narrow. However, for the 1st time in about 2 years, RTY's EPS is outpacing S&P EPS. Maybe more accommodative economic policies are starting to awaken broader parts of the stock market? paulsenperspectives.subtack.com

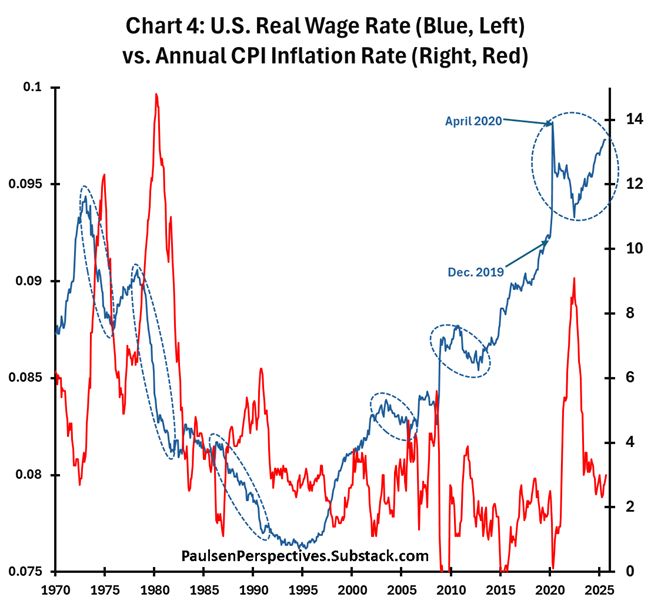

Despite the 2020-2022 inflationary surge being one of the largest in post-war history, among the economy’s major performance benchmarks - real GDP, employment, real profits, & real wages -- there was little damaging impact. Why? See my latest report at paulsenperspectives.substack.com

October 27, 2025 at 11:35 AM

Despite the 2020-2022 inflationary surge being one of the largest in post-war history, among the economy’s major performance benchmarks - real GDP, employment, real profits, & real wages -- there was little damaging impact. Why? See my latest report at paulsenperspectives.substack.com

What has happened to US economic momentum since the government quit releasing econ reports on Oct. 1st? A good proxy for US economic surprises may be the relative performance of S&P cyclical sectors. Cyclicals have continued underperforming badly since Oct 1!

See paulsenperspectives.substack.com

See paulsenperspectives.substack.com

October 24, 2025 at 5:34 PM

What has happened to US economic momentum since the government quit releasing econ reports on Oct. 1st? A good proxy for US economic surprises may be the relative performance of S&P cyclical sectors. Cyclicals have continued underperforming badly since Oct 1!

See paulsenperspectives.substack.com

See paulsenperspectives.substack.com

New-era has carried investors during the first three years of this bull market. Could old-era segments assisted by economic policy easing finally take leadership and elongate this bull for a few more years? See my latest report @ paulsenperspectives.substack.com

October 6, 2025 at 11:56 AM

New-era has carried investors during the first three years of this bull market. Could old-era segments assisted by economic policy easing finally take leadership and elongate this bull for a few more years? See my latest report @ paulsenperspectives.substack.com

Because the jobs market has been so weak, it's become the most important economic metric. Less than 1% job growth in the last year and a rise in the UR make job market conditions simply unacceptable. See my latest free report "Jobs Rule" @ paulsenperspectives.substack.com

October 2, 2025 at 12:04 PM

Because the jobs market has been so weak, it's become the most important economic metric. Less than 1% job growth in the last year and a rise in the UR make job market conditions simply unacceptable. See my latest free report "Jobs Rule" @ paulsenperspectives.substack.com

I recently had the great opportunity to work with Jack Forehand and Justin Carbonneau from the Excess Return Podcast for our monthly discuss. I hope you have some time to Please watch the discussion. Thanks! www.google.com/url?sa=t&rct...

See my reserach @ paulsenperspectives.substack.com

See my reserach @ paulsenperspectives.substack.com

You're Misreading This Bull Market | Jim Paulsen on the Major Supports That Are About to Flip

Follow Jim at https://paulsenperspectives.substack.com/ In this episode, we sit down with Jim Paulsen to analyze the latest economic and market data through his lens of decades of market experience. Jim shares insights from his Paulsen Perspectives research, covering the job market, the Fed, inflation, valuations, investor confidence, and what they all mean for the future of the economy and markets. We explore why confidence is so low despite a bull market, how Fed policy is shaping market dynamics, and where investors might want to focus as the cycle evolves. Topics covered in the episode: * The job market’s pivotal role in driving the economy and Fed decisions * Why recent Fed rate cuts may mark a turning point in market support systems * The narrowness of the bull market and how innovation-driven firms diverge from traditional cycles * Investor confidence, the “misery index,” and recession probability models * How easing may broaden market participation beyond large-cap growth * What “animal spirits” mean for small caps, high beta, and IPOs * The disconnect between inflation, bond yields, and growth measures * Gold, cash, crypto, and tech as “fear assets” in today’s environment * The impact of tariffs on profits, wages, and inflation expectations * Valuations in context: historical perspective and the upward bias of multiples Timestamps: 00:00 Introduction and market overview 02:00 Fed easing, inflation, and recession risks 09:00 Bull market without normal supports 17:00 Narrow leadership and innovative companies 23:55 Confidence and the misery index 29:35 Yield curve, recession probabilities, and Fed policy 34:00 Broadening of market participation 37:00 Animal spirit stocks and small caps 38:00 Inflation, bond yields, and resource unemployment 43:20 Copper-gold ratio and yields 45:10 The role of gold in portfolios 50:00 Cash, crypto, and tech as defensive assets 54:00 Tariffs, inflation, and profit margins 59:00 Inflation persistence vs. wage growth 01:01:10 Valuations and the upward bias in multiples 01:07:00 Closing thoughts and takeaways

www.google.com

October 1, 2025 at 7:16 PM

I recently had the great opportunity to work with Jack Forehand and Justin Carbonneau from the Excess Return Podcast for our monthly discuss. I hope you have some time to Please watch the discussion. Thanks! www.google.com/url?sa=t&rct...

See my reserach @ paulsenperspectives.substack.com

See my reserach @ paulsenperspectives.substack.com

I suspect the disinflationary force from weakness in real economic activities will more than offset any additional inflationary force from tariffs. The chart below shows the average growth of 7 key metrics relative to CPI inflation. See my full report @ paulsenperspectives.substack.com

September 25, 2025 at 12:24 PM

I suspect the disinflationary force from weakness in real economic activities will more than offset any additional inflationary force from tariffs. The chart below shows the average growth of 7 key metrics relative to CPI inflation. See my full report @ paulsenperspectives.substack.com