Shane Phillips

@shanedphillips.bsky.social

Housing guy. Researcher at UCLA Lewis Center, host of UCLA Housing Voice Podcast, author of The Affordable City, resident of Los Angeles.

My favorite part of the tariffs is how, in addition to the tax itself, I also get to pay an even larger fee to the broker. More than doubling the additional cost to me, the consumer.

January 21, 2026 at 8:16 PM

My favorite part of the tariffs is how, in addition to the tax itself, I also get to pay an even larger fee to the broker. More than doubling the additional cost to me, the consumer.

...that drove up rents, and that disproportionately hurt lower and middle-income households and communities. (The black line in this chart is price-to-income in a low-income Atlanta census tract; the red line is a high-income tract.)

January 21, 2026 at 6:43 PM

...that drove up rents, and that disproportionately hurt lower and middle-income households and communities. (The black line in this chart is price-to-income in a low-income Atlanta census tract; the red line is a high-income tract.)

The result was a post-2008 crash that was much deeper and longer-lasting than it had to be, that decimated the construction industry even as it kept growing in peer countries like Canada and Australia, that dramatically shrank the market for new construction...

January 21, 2026 at 6:43 PM

The result was a post-2008 crash that was much deeper and longer-lasting than it had to be, that decimated the construction industry even as it kept growing in peer countries like Canada and Australia, that dramatically shrank the market for new construction...

Tightening of lending standards leading up to and following the crash ended up shutting out roughly a third of the conventional mortgage borrowers — mostly people with good credit scores and low borrower risk.

January 21, 2026 at 6:43 PM

Tightening of lending standards leading up to and following the crash ended up shutting out roughly a third of the conventional mortgage borrowers — mostly people with good credit scores and low borrower risk.

Very strange that LADWP's rebate program for high-efficiencly appliances, thermostats, etc. also applies to TVs. I have to assume almost no one actually claims it since it's so small, but in that case why even have it?

January 8, 2026 at 9:55 PM

Very strange that LADWP's rebate program for high-efficiencly appliances, thermostats, etc. also applies to TVs. I have to assume almost no one actually claims it since it's so small, but in that case why even have it?

These figures really capture the problem — a problem that poorly design construction defect liability laws contribute to, but by no means fully explain. The report that our conversation focuses on is here: ternercenter.berkeley.edu/wp-content/u...

December 18, 2025 at 6:02 PM

These figures really capture the problem — a problem that poorly design construction defect liability laws contribute to, but by no means fully explain. The report that our conversation focuses on is here: ternercenter.berkeley.edu/wp-content/u...

For those interested, here are the model inputs for the different financial models, with "Ideal Loan Product SPR" being the preferred, and the one referenced in results throughout the report. (This table is on page 65 of the report.) The second table (pg. 80) are assumptions for the owner model.

December 8, 2025 at 7:57 PM

For those interested, here are the model inputs for the different financial models, with "Ideal Loan Product SPR" being the preferred, and the one referenced in results throughout the report. (This table is on page 65 of the report.) The second table (pg. 80) are assumptions for the owner model.

I also share this chart because unlike the others, it shows SPR returns only *during* the tenancy—which is why they appear lower than elsewhere. But the comparison to homeownership also shows that they're quite high, especially when we make reasonable assumptions about ownership.

December 8, 2025 at 7:57 PM

I also share this chart because unlike the others, it shows SPR returns only *during* the tenancy—which is why they appear lower than elsewhere. But the comparison to homeownership also shows that they're quite high, especially when we make reasonable assumptions about ownership.

Using relatively simple financial models, the report shows that this housing model could be feasible in some markets, meaning that it produces tenant financial benefits *and* yields competitive returns for project sponsors. Here's a comparison of "returns" for an SPR tenant and typical homeowner.

December 8, 2025 at 7:57 PM

Using relatively simple financial models, the report shows that this housing model could be feasible in some markets, meaning that it produces tenant financial benefits *and* yields competitive returns for project sponsors. Here's a comparison of "returns" for an SPR tenant and typical homeowner.

Behind the idea for SPR housing is the fact that homeownership just isn't the answer for many Americans. Homeowners are much wealthier than renters, but the "homeownership society" has always been unequal and volatile—it hasn't worked for everyone, and it never will.

December 8, 2025 at 7:57 PM

Behind the idea for SPR housing is the fact that homeownership just isn't the answer for many Americans. Homeowners are much wealthier than renters, but the "homeownership society" has always been unequal and volatile—it hasn't worked for everyone, and it never will.

This table (pg. 78) is simpler, but it adds the complexity of expiration policy. It shows the share of rent paid back to tenants based on tenancy length and "rental reward" expiration. Considering SPR housing asks nothing more of renters than traditional rentals, these are big numbers.

December 8, 2025 at 7:57 PM

This table (pg. 78) is simpler, but it adds the complexity of expiration policy. It shows the share of rent paid back to tenants based on tenancy length and "rental reward" expiration. Considering SPR housing asks nothing more of renters than traditional rentals, these are big numbers.

Here's a hypothetical tenant who lives in an SPR unit for 5 years, moves out, and keeps collecting rental reward payments for 10 more years until the last one expires. The chart shows annual rent paid, annual reward payments, and the share of rent ultimately paid back (roughly adj. for inflation).

December 8, 2025 at 7:57 PM

Here's a hypothetical tenant who lives in an SPR unit for 5 years, moves out, and keeps collecting rental reward payments for 10 more years until the last one expires. The chart shows annual rent paid, annual reward payments, and the share of rent ultimately paid back (roughly adj. for inflation).

This figure illustrates how payments work in the model: Every 7 years the project sponsor refinances, and if the property value is growing then this generates revenue to pay both sponsor/investor profits and tenant financial rewards.

December 8, 2025 at 7:57 PM

This figure illustrates how payments work in the model: Every 7 years the project sponsor refinances, and if the property value is growing then this generates revenue to pay both sponsor/investor profits and tenant financial rewards.

In my report with Jason Ward, we looked at transactions of properties with high-density zoning and low-intensity uses as a leading indicator of redevelopment, also finding a 50% drop in LA sales relative to other LA County jurisdictions. As above, that trend has persisted over the past 6 months.

November 26, 2025 at 7:00 PM

In my report with Jason Ward, we looked at transactions of properties with high-density zoning and low-intensity uses as a leading indicator of redevelopment, also finding a 50% drop in LA sales relative to other LA County jurisdictions. As above, that trend has persisted over the past 6 months.

Sales also haven't shown much sign of recovering. Mike Manville and Mott Smith evaluated ULA's impact on sales over $5 million and on property tax revenue. Their study period ended with Q4 2024, but newer data shows the gap between LA and the rest of the county has actually widened since then.

November 26, 2025 at 7:00 PM

Sales also haven't shown much sign of recovering. Mike Manville and Mott Smith evaluated ULA's impact on sales over $5 million and on property tax revenue. Their study period ended with Q4 2024, but newer data shows the gap between LA and the rest of the county has actually widened since then.

Maybe production is recovering, but there's not much data to support that conclusion yet — unless you use it dishonestly. If we look at annual figures, which smooth out some of the quarterly variability, 2025 looks about as bad as 2024, which itself was historically bad.

November 26, 2025 at 7:00 PM

Maybe production is recovering, but there's not much data to support that conclusion yet — unless you use it dishonestly. If we look at annual figures, which smooth out some of the quarterly variability, 2025 looks about as bad as 2024, which itself was historically bad.

The group also says permits rose quarter-over-quarter through 2025. Again, true but misleading, and for a similar reason. This chart shows quarterly permitting through Q3 2025, with Q1 2025 circled. This is their baseline for this claim — the worst quarter in 5 years. That's point two.

November 26, 2025 at 7:00 PM

The group also says permits rose quarter-over-quarter through 2025. Again, true but misleading, and for a similar reason. This chart shows quarterly permitting through Q3 2025, with Q1 2025 circled. This is their baseline for this claim — the worst quarter in 5 years. That's point two.

First, the statement that permits are up 60% in the 3rd quarter. This is is true but misleading. Why? Because up to that date, Q3 2024 was the worst quarter for housing construction permits since before 2020. My chart (the 2nd one) illustrates this: the area circled in red is their baseline.

November 26, 2025 at 7:00 PM

First, the statement that permits are up 60% in the 3rd quarter. This is is true but misleading. Why? Because up to that date, Q3 2024 was the worst quarter for housing construction permits since before 2020. My chart (the 2nd one) illustrates this: the area circled in red is their baseline.

Since October, Measure ULA advocates have been sharing this data showing a 60% increase in permitted units in Q3 2025 compared to Q3 2024. It's intended as evidence that the tax's impact on production, documented in our Taxing Tomorrow report, is transitory. A thread on why this is misleading. 🧵

November 26, 2025 at 7:00 PM

Since October, Measure ULA advocates have been sharing this data showing a 60% increase in permitted units in Q3 2025 compared to Q3 2024. It's intended as evidence that the tax's impact on production, documented in our Taxing Tomorrow report, is transitory. A thread on why this is misleading. 🧵

This paragraph brings great joy to my heart. If only we should all be so fortunate.

cc: @resnikoff.bsky.social

cc: @resnikoff.bsky.social

![Screenshot of text from Wikipedia: "The Commonwealth of Massachusetts has 14 counties, though eight[1] of these fourteen county governments were abolished between 1997 and 2000. The counties in the southeastern portion of the state retain county-level local government (Barnstable, Bristol, Dukes, Norfolk, Plymouth) or, in one case, (Nantucket County) consolidated town-county government.[2][3] Vestigial judicial and law enforcement districts still follow county boundaries even in the counties whose county-level government has been disestablished, and the counties are still generally recognized as geographic entities if not political ones.[4] Three counties (Hampshire, Barnstable, and Franklin) have formed new county regional compacts to serve as a form of regional governance."](https://cdn.bsky.app/img/feed_thumbnail/plain/did:plc:mcarhragq2bw4wzlu3tdbubf/bafkreiaewustcg2pmyibvmgmj2p4qtpivbtem3cewwhoshxetnrc7lx4ti@jpeg)

October 6, 2025 at 3:35 AM

This paragraph brings great joy to my heart. If only we should all be so fortunate.

cc: @resnikoff.bsky.social

cc: @resnikoff.bsky.social

Tag yourself I'm Mount Whoredom

October 4, 2025 at 9:28 PM

Tag yourself I'm Mount Whoredom

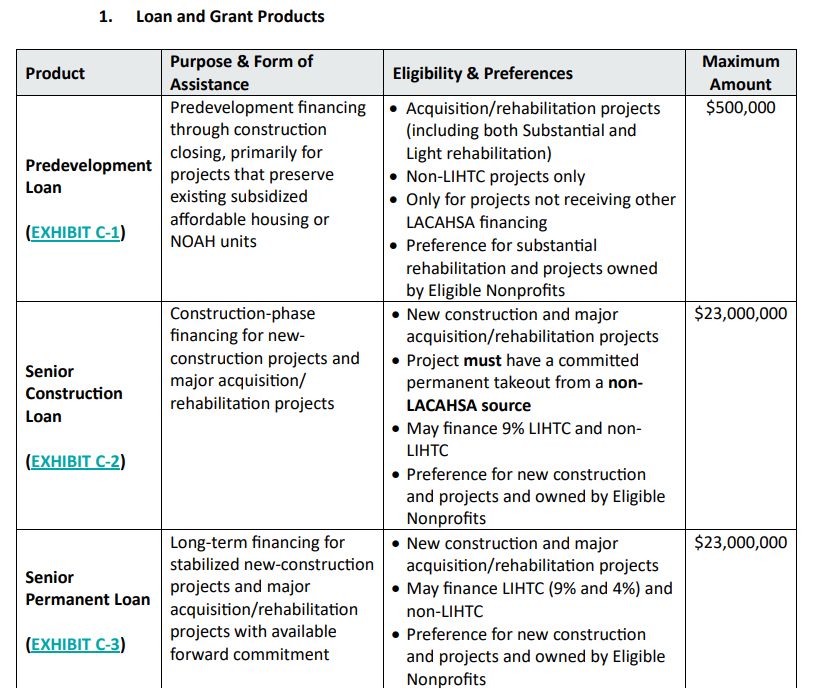

As an example, it *seems* to me that issuing permanent loans is a poor use of limited agency funds (~$200MM for this NOFA). Couldn't banks do this, even if it's a bit more expensive? Wouldn't that money be tied up for decades? But I don't know if these are actually valid concerns.

October 1, 2025 at 3:56 PM

As an example, it *seems* to me that issuing permanent loans is a poor use of limited agency funds (~$200MM for this NOFA). Couldn't banks do this, even if it's a bit more expensive? Wouldn't that money be tied up for decades? But I don't know if these are actually valid concerns.

Having fewer elevators means more people live in multi-story buildings where their only means of accessing their unit is the stairs. That's a disaster for anyone with mobility challenges. Buildings like this one in Spain, which has 3 stories, 54 units, and 9 elevators, are completely unheard of.

September 24, 2025 at 7:07 PM

Having fewer elevators means more people live in multi-story buildings where their only means of accessing their unit is the stairs. That's a disaster for anyone with mobility challenges. Buildings like this one in Spain, which has 3 stories, 54 units, and 9 elevators, are completely unheard of.