Alessandro Rebucci

@arebucci.bsky.social

150 followers

24 following

40 posts

Professor of Economics and Finance at Johns Hopkins Carey Business School. International finance and macroeconomics. Former IMF and IDB.

https://carey.jhu.edu/faculty/faculty-directory/alessandro-rebucci-phd

Posts

Media

Videos

Starter Packs

Alessandro Rebucci

@arebucci.bsky.social

· May 13

Reposted by Alessandro Rebucci

Alessandro Rebucci

@arebucci.bsky.social

· Apr 21

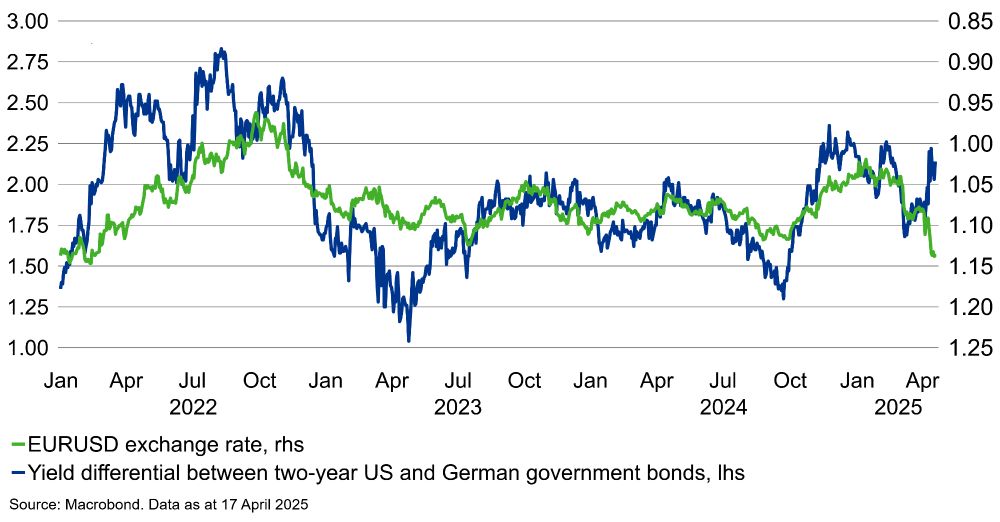

Tariffs, the dollar, and equities: High-frequency evidence from the Liberation Day announcement

On 2 April 2025, the US announced tariffs on most of its trading partners, creating a major trade policy shock to the world economy. This column shows that the US dollar depreciated on impact, rather than appreciating as expected based on standard theory and prior evidence. The authors argue that this unusual transmission impact of the tariffs on the dollar was driven by foreign equity portfolio rebalancing away from US equities. US trade policy not only needs to consider possible impacts on US safe assets but also risky assets.

cepr.org

Alessandro Rebucci

@arebucci.bsky.social

· Apr 21

Alessandro Rebucci

@arebucci.bsky.social

· Apr 21

Reposted by Alessandro Rebucci

Alessandro Rebucci

@arebucci.bsky.social

· Apr 17

Once-Hot Wall Street Funds Unravel Fast With No Savior in Sight

With Jerome Powell ruling out a rescue mission this week and incurring the wrath of Donald Trump, Wall Street is desperate for a lifeline as tariff-lashed markets slide anew.

www.bloomberg.com

Alessandro Rebucci

@arebucci.bsky.social

· Apr 17

Alessandro Rebucci

@arebucci.bsky.social

· Apr 17

Alessandro Rebucci

@arebucci.bsky.social

· Apr 17

Input Specificity and the Propagation of Idiosyncratic Shocks in Production Networks *

Abstract. This article examines whether firm-level idiosyncratic shocks propagate in production networks. We identify idiosyncratic shocks with the occurre

academic.oup.com

Alessandro Rebucci

@arebucci.bsky.social

· Apr 17

Tariffs, the dollar, and equities: High-frequency evidence from the Liberation Day announcement

On 2 April 2025, the US announced tariffs on most of its trading partners, creating a major trade policy shock to the world economy. This column shows that the US dollar depreciated on impact, rather than appreciating as expected based on standard theory and prior evidence. The authors argue that this unusual transmission impact of the tariffs on the dollar was driven by foreign equity portfolio rebalancing away from US equities. US trade policy not only needs to consider possible impacts on US safe assets but also risky assets.

cepr.org

Alessandro Rebucci

@arebucci.bsky.social

· Apr 16