Jonathan Heathcote

@heathcote.bsky.social

2.6K followers

660 following

29 posts

Economist. Macro, inequality, public finance, international finance, asset pricing, labor.

https://www.jonathanheathcote.com

Posts

Media

Videos

Starter Packs

Reposted by Jonathan Heathcote

Reposted by Jonathan Heathcote

Jonathan Heathcote

@heathcote.bsky.social

· Feb 11

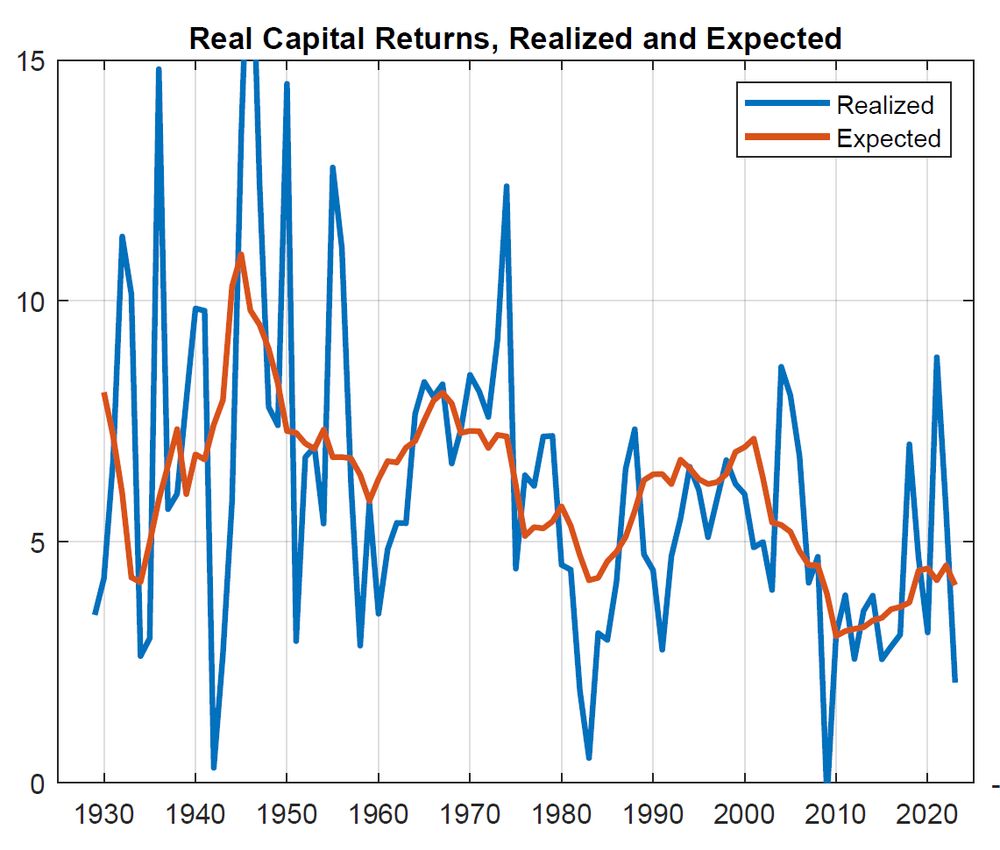

Reconciling Macroeconomics and Finance for the U.S. Corporate Sector: 1929 to Present

Founded in 1920, the NBER is a private, non-profit, non-partisan organization dedicated to conducting economic research and to disseminating research findings among academics, public policy makers, an...

www.nber.org

Jonathan Heathcote

@heathcote.bsky.social

· Feb 11

Jonathan Heathcote

@heathcote.bsky.social

· Feb 11

Jonathan Heathcote

@heathcote.bsky.social

· Feb 11

Jonathan Heathcote

@heathcote.bsky.social

· Feb 11

Reconciling Macroeconomics and Finance for the U.S. Corporate Sector: 1929 to Present

Founded in 1920, the NBER is a private, non-profit, non-partisan organization dedicated to conducting economic research and to disseminating research findings among academics, public policy makers, an...

www.nber.org

Jonathan Heathcote

@heathcote.bsky.social

· Jan 14

Jonathan Heathcote

@heathcote.bsky.social

· Jan 12

Jonathan Heathcote

@heathcote.bsky.social

· Jan 12

Jonathan Heathcote

@heathcote.bsky.social

· Jan 12

Reposted by Jonathan Heathcote

Reposted by Jonathan Heathcote

Jonathan Heathcote

@heathcote.bsky.social

· Dec 14

Jonathan Heathcote

@heathcote.bsky.social

· Dec 10

Reposted by Jonathan Heathcote