Marco Garofalo

@marcogarofalo.bsky.social

98 followers

120 following

22 posts

Senior economist @bankofengland PhD student @OxfordEconDept @UniofOxford ⚽️ Long-suffering AS Roma fan 🇮🇹🇳🇱🇪🇺🇬🇧 RTs ≠ endorsements, any views my own.

Website: https://sites.google.com/view/marco-garofalo/home

Posts

Media

Videos

Starter Packs

Pinned

Reposted by Marco Garofalo

Reposted by Marco Garofalo

Chatham House

@chathamhouse.org

· Jun 6

Ukraine’s Operation Spider’s Web is a game-changer for modern drone warfare. NATO should pay attention

The use of cheap drones to strike targets deep within Russia provides a blueprint for rapidly evolving modern warfare that should inform how states seek to defend themselves.

www.chathamhouse.org

Reposted by Marco Garofalo

Reposted by Marco Garofalo

Marco Garofalo

@marcogarofalo.bsky.social

· Apr 15

Marco Garofalo

@marcogarofalo.bsky.social

· Apr 15

Marco Garofalo

@marcogarofalo.bsky.social

· Apr 15

Marco Garofalo

@marcogarofalo.bsky.social

· Apr 15

Marco Garofalo

@marcogarofalo.bsky.social

· Apr 15

Marco Garofalo

@marcogarofalo.bsky.social

· Apr 15

Reposted by Marco Garofalo

Reposted by Marco Garofalo

Reposted by Marco Garofalo

Reposted by Marco Garofalo

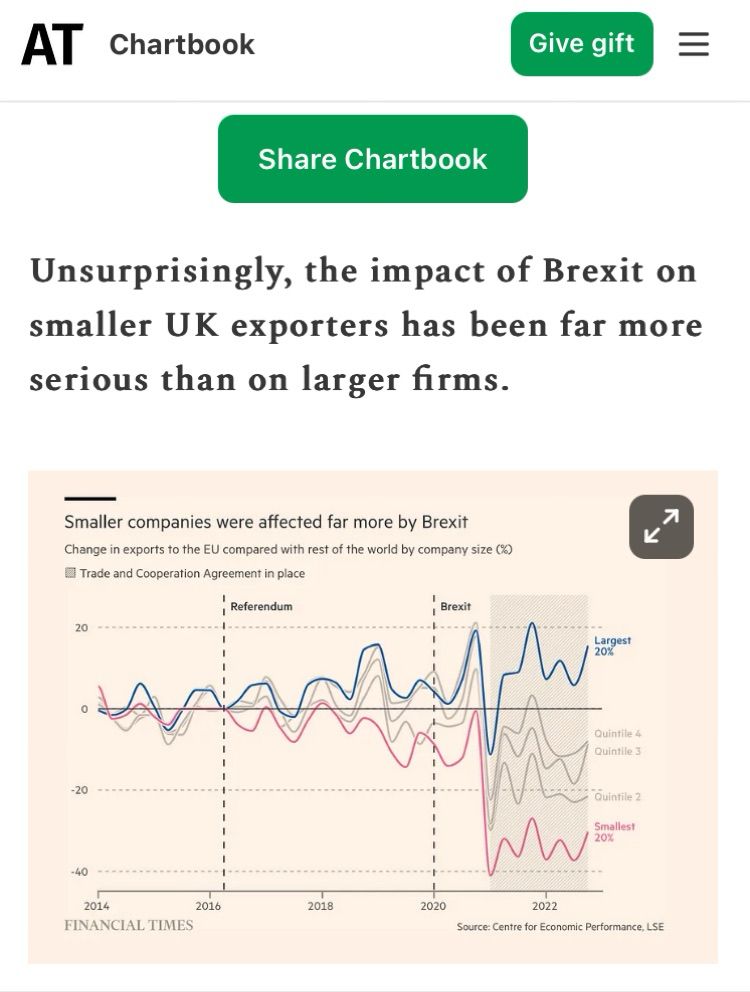

Marco Garofalo

@marcogarofalo.bsky.social

· Mar 12

Deep integration and trade: UK firms in the wake of Brexit - ORA - Oxford University Research Archive

How does dismantling deep integration affect international trade? This paper provides new evidence on the consequences of disintegration by estimating the impact of Brexit on goods trade by UK firms. The UK’s exit from the EU’s single market and customs union in January 2021 led to an immediate,

ora.ox.ac.uk