@ttunguz.bsky.social

Google is leading the deflation in AI pricing, selling tremendous performance at going-out-of-business prices.

State of the art (SOTA) : the best score achieved by any model on a given benchmark, used as the 100% baseline. Performance score = 100 + average percentage delta from SOTA.

State of the art (SOTA) : the best score achieved by any model on a given benchmark, used as the 100% baseline. Performance score = 100 + average percentage delta from SOTA.

December 17, 2025 at 10:57 PM

Google is leading the deflation in AI pricing, selling tremendous performance at going-out-of-business prices.

State of the art (SOTA) : the best score achieved by any model on a given benchmark, used as the 100% baseline. Performance score = 100 + average percentage delta from SOTA.

State of the art (SOTA) : the best score achieved by any model on a given benchmark, used as the 100% baseline. Performance score = 100 + average percentage delta from SOTA.

Gemini 3 Flash compresses what took $65 of GPT-4 tokens in March 2023 into $1.10 today for equivalent capability. That’s 98% deflation in 33 months. For teams building AI products, this isn’t incremental improvement : it’s a category shift that makes previously uneconomic use cases viable.

December 17, 2025 at 10:57 PM

Gemini 3 Flash compresses what took $65 of GPT-4 tokens in March 2023 into $1.10 today for equivalent capability. That’s 98% deflation in 33 months. For teams building AI products, this isn’t incremental improvement : it’s a category shift that makes previously uneconomic use cases viable.

Third, output price-performance. The spread widens further. Gemini 3 Flash scores 30.3 performance points per output dollar versus Claude Opus 4.5’s 3.5 points. Claude charges $25 per million output tokens : 8x more than Gemini’s $3 : while scoring 2.6% lower on aggregate benchmarks.

December 17, 2025 at 10:57 PM

Third, output price-performance. The spread widens further. Gemini 3 Flash scores 30.3 performance points per output dollar versus Claude Opus 4.5’s 3.5 points. Claude charges $25 per million output tokens : 8x more than Gemini’s $3 : while scoring 2.6% lower on aggregate benchmarks.

Second, input price-performance. Looking at overall price-performance by input tokens reveals a huge gap. Gemini 3 Flash delivers 182 performance points per dollar compared to GPT-5.2 at 53. That’s a 3.4x advantage.

December 17, 2025 at 10:57 PM

Second, input price-performance. Looking at overall price-performance by input tokens reveals a huge gap. Gemini 3 Flash delivers 182 performance points per dollar compared to GPT-5.2 at 53. That’s a 3.4x advantage.

How much better is the price-performance? How much cheaper can teams run inference?

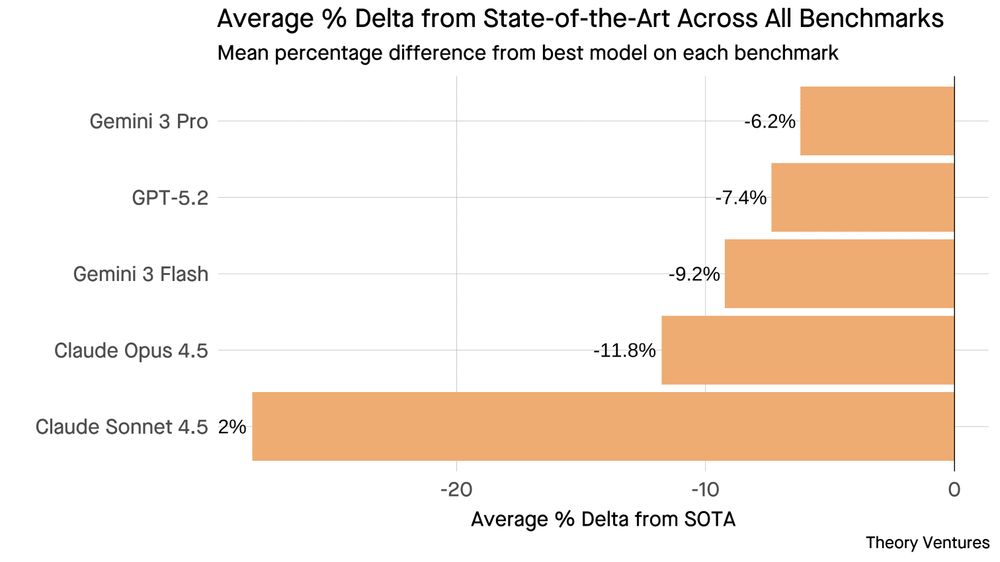

First, performance. Gemini 3 Pro tops this analysis with a 6% deviation from state of the art. Gemini 3 Flash is not far behind at 9%, followed by Opus at 12%.

First, performance. Gemini 3 Pro tops this analysis with a 6% deviation from state of the art. Gemini 3 Flash is not far behind at 9%, followed by Opus at 12%.

December 17, 2025 at 10:57 PM

How much better is the price-performance? How much cheaper can teams run inference?

First, performance. Gemini 3 Pro tops this analysis with a 6% deviation from state of the art. Gemini 3 Flash is not far behind at 9%, followed by Opus at 12%.

First, performance. Gemini 3 Pro tops this analysis with a 6% deviation from state of the art. Gemini 3 Flash is not far behind at 9%, followed by Opus at 12%.

The chart below contrasts retention across leading models. Claude 4 Sonnet & Gemini 2.5 Flash show stronger Month 1 retention (40-50%) compared to GPT-4o Mini & DeepSeek R1 (25-35%), suggesting deeper utility for certain workflows.

December 16, 2025 at 10:42 PM

The chart below contrasts retention across leading models. Claude 4 Sonnet & Gemini 2.5 Flash show stronger Month 1 retention (40-50%) compared to GPT-4o Mini & DeepSeek R1 (25-35%), suggesting deeper utility for certain workflows.

Third, coding has found product-market fit. Programming accounts for 60% of Anthropic’s usage & 45% of xAI’s, both heavily skewed toward developer workflows.

The table below shows the top 2 use cases by provider (November 2025). Technology refers to AI assistant tasks like research & summarization.

The table below shows the top 2 use cases by provider (November 2025). Technology refers to AI assistant tasks like research & summarization.

December 16, 2025 at 10:42 PM

Third, coding has found product-market fit. Programming accounts for 60% of Anthropic’s usage & 45% of xAI’s, both heavily skewed toward developer workflows.

The table below shows the top 2 use cases by provider (November 2025). Technology refers to AI assistant tasks like research & summarization.

The table below shows the top 2 use cases by provider (November 2025). Technology refers to AI assistant tasks like research & summarization.

Second, the distribution of open-source models has shifted dramatically. DeepSeek held nearly 80% of OSS market share in early 2025, but has dropped to 40% as Qwen & other Chinese models have gained ground.

December 16, 2025 at 10:42 PM

Second, the distribution of open-source models has shifted dramatically. DeepSeek held nearly 80% of OSS market share in early 2025, but has dropped to 40% as Qwen & other Chinese models have gained ground.

The weak price elasticity indicates that even drastic cost differences do not fully shift demand; proprietary providers retain pricing power for mission-critical applications, while open ecosystems absorb volume from cost-sensitive users.

December 16, 2025 at 10:42 PM

The weak price elasticity indicates that even drastic cost differences do not fully shift demand; proprietary providers retain pricing power for mission-critical applications, while open ecosystems absorb volume from cost-sensitive users.

The Balance Sheet Arbitrage

December 15, 2025 at 6:37 PM

The Balance Sheet Arbitrage

Meta-Blue Owl Hyperion Joint Venture

Meta took this even further in October 2025 with Blue Owl Capital :

Meta took this even further in October 2025 with Blue Owl Capital :

December 15, 2025 at 6:37 PM

Meta-Blue Owl Hyperion Joint Venture

Meta took this even further in October 2025 with Blue Owl Capital :

Meta took this even further in October 2025 with Blue Owl Capital :

With this deal, BlackRock GIP + Microsoft now matches Blackstone as the largest data center acquirer, each with ~$40B in total deal value since 2021.

Why this structure matters : The 70% debt leverage sits at the fund level, not on Microsoft’s corporate balance sheet.

Why this structure matters : The 70% debt leverage sits at the fund level, not on Microsoft’s corporate balance sheet.

December 15, 2025 at 6:37 PM

With this deal, BlackRock GIP + Microsoft now matches Blackstone as the largest data center acquirer, each with ~$40B in total deal value since 2021.

Why this structure matters : The 70% debt leverage sits at the fund level, not on Microsoft’s corporate balance sheet.

Why this structure matters : The 70% debt leverage sits at the fund level, not on Microsoft’s corporate balance sheet.

Microsoft-BlackRock AI Infrastructure Partnership (AIP)

In September 2024, BlackRock, Global Infrastructure Partners (GIP), Microsoft, & MGX launched the AI Infrastructure Partnership with a distinctive financing structure.

In September 2024, BlackRock, Global Infrastructure Partners (GIP), Microsoft, & MGX launched the AI Infrastructure Partnership with a distinctive financing structure.

December 15, 2025 at 6:37 PM

Microsoft-BlackRock AI Infrastructure Partnership (AIP)

In September 2024, BlackRock, Global Infrastructure Partners (GIP), Microsoft, & MGX launched the AI Infrastructure Partnership with a distinctive financing structure.

In September 2024, BlackRock, Global Infrastructure Partners (GIP), Microsoft, & MGX launched the AI Infrastructure Partnership with a distinctive financing structure.

Oracle’s leverage is 20+ times higher than Microsoft & Google, despite generating only a fraction of their revenue. The company carries $100 billion in total debt while operating at a fundamentally different scale than the hyperscalers it’s trying to compete against.

December 15, 2025 at 6:37 PM

Oracle’s leverage is 20+ times higher than Microsoft & Google, despite generating only a fraction of their revenue. The company carries $100 billion in total debt while operating at a fundamentally different scale than the hyperscalers it’s trying to compete against.

The Leverage Problem

Oracle’s debt-to-equity ratio has ballooned to 500%, dwarfing its cloud computing peers.

Oracle’s debt-to-equity ratio has ballooned to 500%, dwarfing its cloud computing peers.

December 15, 2025 at 6:37 PM

The Leverage Problem

Oracle’s debt-to-equity ratio has ballooned to 500%, dwarfing its cloud computing peers.

Oracle’s debt-to-equity ratio has ballooned to 500%, dwarfing its cloud computing peers.

More telling, however, are the credit default swaps.

December 15, 2025 at 6:37 PM

More telling, however, are the credit default swaps.

Despite record-breaking remaining performance obligation (RPO) growth of 438% to $523 billion, actual revenue has not increased as quickly as hoped.

December 15, 2025 at 6:37 PM

Despite record-breaking remaining performance obligation (RPO) growth of 438% to $523 billion, actual revenue has not increased as quickly as hoped.

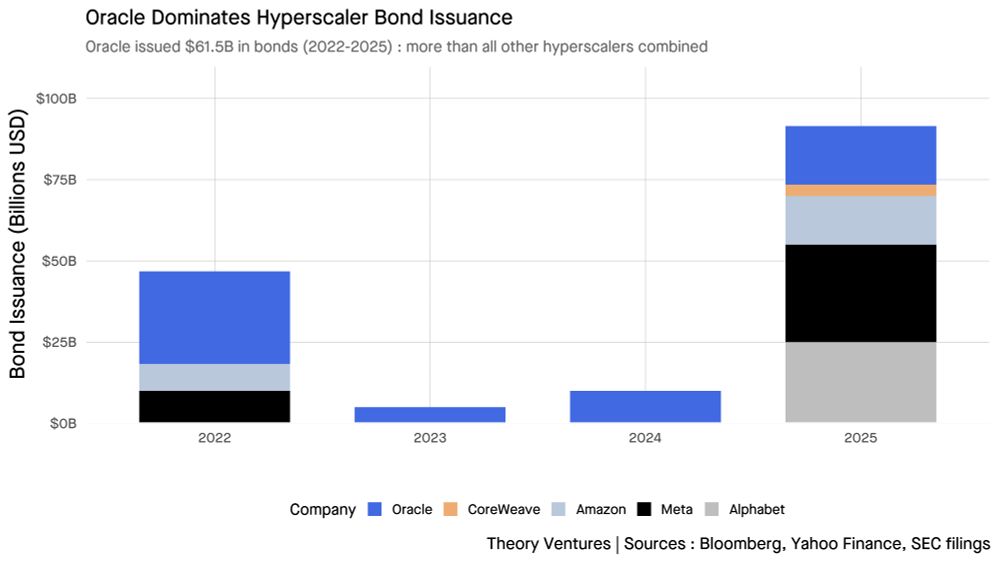

In 2025 alone, hyperscalers issued $121 billion in bonds, more than four times the five-year average of $28 billion. Oracle led with $61.5 billion total across 2022-2025, driven by its $28.5 billion Cerner acquisition financing & $18 billion AI infrastructure raise.

December 15, 2025 at 6:37 PM

In 2025 alone, hyperscalers issued $121 billion in bonds, more than four times the five-year average of $28 billion. Oracle led with $61.5 billion total across 2022-2025, driven by its $28.5 billion Cerner acquisition financing & $18 billion AI infrastructure raise.

Recently Oracle’s bonds have been weighing on my mind.

AI’s capital expenditure in 2025 represents about 1.6% of US GDP. In 2026, that number should top 3% of US GDP according to Goldman Sachs estimates.

AI’s capital expenditure in 2025 represents about 1.6% of US GDP. In 2026, that number should top 3% of US GDP according to Goldman Sachs estimates.

December 15, 2025 at 6:37 PM

Recently Oracle’s bonds have been weighing on my mind.

AI’s capital expenditure in 2025 represents about 1.6% of US GDP. In 2026, that number should top 3% of US GDP according to Goldman Sachs estimates.

AI’s capital expenditure in 2025 represents about 1.6% of US GDP. In 2026, that number should top 3% of US GDP according to Goldman Sachs estimates.

Third, press coverage distorts perception. Media tends to spotlight younger founders pursuing product-led growth or consumer strategies. The Cursor team, fresh from MIT, captures the zeitgeist. But there are many founders who grow up within an industry & then go out to upend it.

December 12, 2025 at 8:38 PM

Third, press coverage distorts perception. Media tends to spotlight younger founders pursuing product-led growth or consumer strategies. The Cursor team, fresh from MIT, captures the zeitgeist. But there are many founders who grow up within an industry & then go out to upend it.

I suspect founder age has been increasing steadily for three reasons. First, venture capital has shifted toward AI, which grew from roughly 10% to 60% of investment in just three years.

December 12, 2025 at 8:38 PM

I suspect founder age has been increasing steadily for three reasons. First, venture capital has shifted toward AI, which grew from roughly 10% to 60% of investment in just three years.

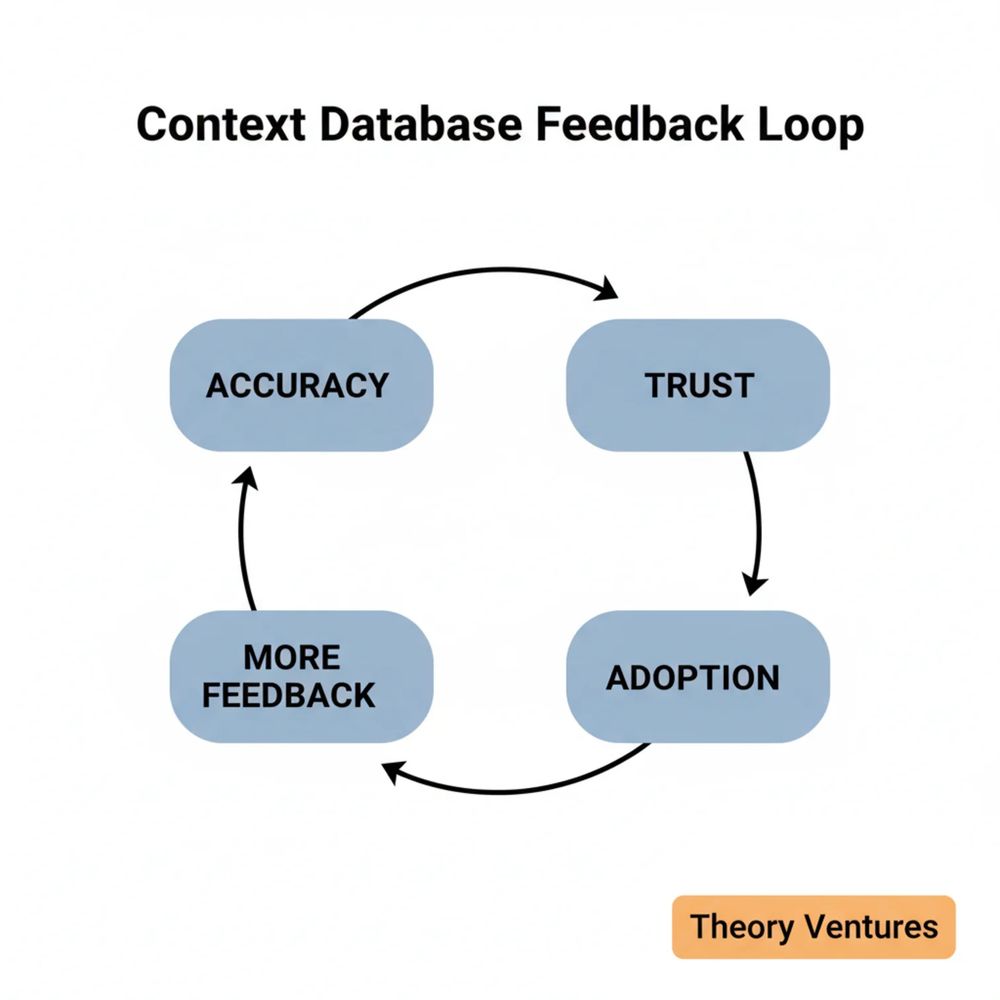

Context databases enable the future of process automation, representing the real promise of AI within the workforce. It’s the evolution of RPA (robotic process automation), but it’s RPA & process discovery injected with non-determinism.

December 10, 2025 at 8:15 PM

Context databases enable the future of process automation, representing the real promise of AI within the workforce. It’s the evolution of RPA (robotic process automation), but it’s RPA & process discovery injected with non-determinism.

Leaders have recognized their companies need a new system of record for AI agents in the form of a context database. There are two different kinds of these context databases :

December 10, 2025 at 8:15 PM

Leaders have recognized their companies need a new system of record for AI agents in the form of a context database. There are two different kinds of these context databases :

Current AI pricing captures between 3% & 5% of this value :

December 9, 2025 at 6:10 PM

Current AI pricing captures between 3% & 5% of this value :

A major question for Confluent over the last few quarters has been : what is the next adjacent product category to catapult another wave of growth? The AI surge has been a positive for the company.

December 8, 2025 at 8:31 PM

A major question for Confluent over the last few quarters has been : what is the next adjacent product category to catapult another wave of growth? The AI surge has been a positive for the company.