Zhexun Mo

@zhexunmo.bsky.social

Postdoc - @stone-lis.bsky.social | East Asia Coordinator - World Inequality Lab | Ph.D. - @pse.bsky.social | Political/Public Econ + Econ History + Development of China, East Asia and Africa | Chasing Inequalities 🏳️🌈 https://sites.google.com/view/zhexunmo

📌 Heterogeneity:

Quantile regressions on WTA measures show that fact-checking and positive narratives reduce the penalty only among respondents already at the favorable end.

Heavy baseline bias → no treatment response

Low baseline bias → clear treatment effect to information and narratives

Quantile regressions on WTA measures show that fact-checking and positive narratives reduce the penalty only among respondents already at the favorable end.

Heavy baseline bias → no treatment response

Low baseline bias → clear treatment effect to information and narratives

November 22, 2025 at 2:37 AM

📌 Heterogeneity:

Quantile regressions on WTA measures show that fact-checking and positive narratives reduce the penalty only among respondents already at the favorable end.

Heavy baseline bias → no treatment response

Low baseline bias → clear treatment effect to information and narratives

Quantile regressions on WTA measures show that fact-checking and positive narratives reduce the penalty only among respondents already at the favorable end.

Heavy baseline bias → no treatment response

Low baseline bias → clear treatment effect to information and narratives

📉 More on Willingness-To-Accept (WTA):

To consider a Chinese investor equivalent to an EU/US investor, respondents require more job preservation:

• EU/US investor baseline: 250 jobs saved

• Chinese investor: ~350 jobs saved

This implies a ~50% China-origin penalty built into public preferences.

To consider a Chinese investor equivalent to an EU/US investor, respondents require more job preservation:

• EU/US investor baseline: 250 jobs saved

• Chinese investor: ~350 jobs saved

This implies a ~50% China-origin penalty built into public preferences.

November 22, 2025 at 2:34 AM

📉 More on Willingness-To-Accept (WTA):

To consider a Chinese investor equivalent to an EU/US investor, respondents require more job preservation:

• EU/US investor baseline: 250 jobs saved

• Chinese investor: ~350 jobs saved

This implies a ~50% China-origin penalty built into public preferences.

To consider a Chinese investor equivalent to an EU/US investor, respondents require more job preservation:

• EU/US investor baseline: 250 jobs saved

• Chinese investor: ~350 jobs saved

This implies a ~50% China-origin penalty built into public preferences.

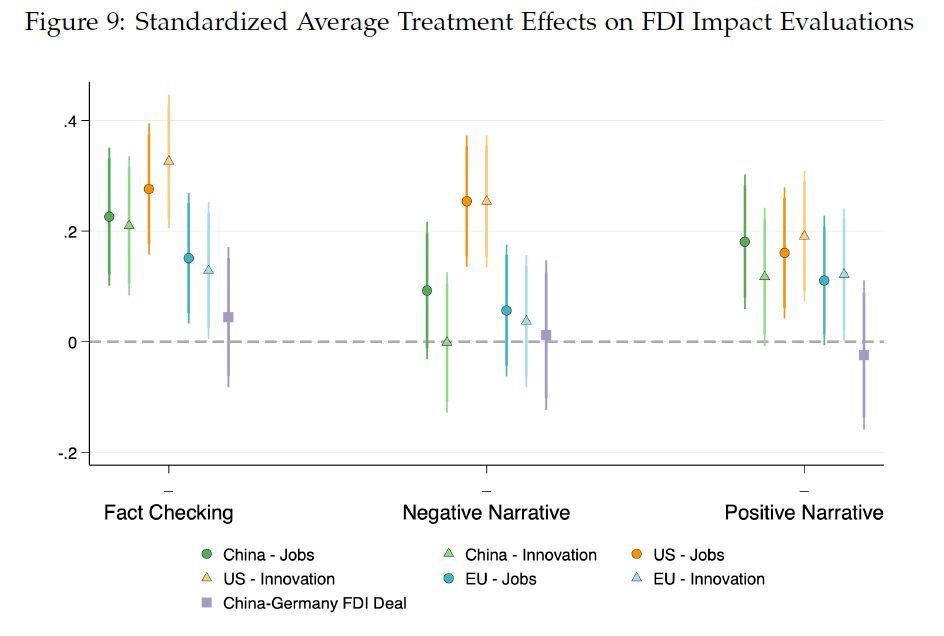

📈 Fact-checking effects:

Providing accurate information significantly improves perceived economic benefits of FDI (across the board regardless of the country of origin) — by roughly 0.2–0.3 standard deviations

Providing accurate information significantly improves perceived economic benefits of FDI (across the board regardless of the country of origin) — by roughly 0.2–0.3 standard deviations

November 22, 2025 at 2:30 AM

📈 Fact-checking effects:

Providing accurate information significantly improves perceived economic benefits of FDI (across the board regardless of the country of origin) — by roughly 0.2–0.3 standard deviations

Providing accurate information significantly improves perceived economic benefits of FDI (across the board regardless of the country of origin) — by roughly 0.2–0.3 standard deviations

🇨🇳➡️🇩🇪 Meanwhile in China:

Chinese respondents express overwhelmingly positive evaluations of German FDI, rating it highly on:

✔️ job creation

✔️ technological upgrading

✔️ national economic development

Roughly 80% provide strongly favorable assessments.

The asymmetry in mutual perceptions is striking.

Chinese respondents express overwhelmingly positive evaluations of German FDI, rating it highly on:

✔️ job creation

✔️ technological upgrading

✔️ national economic development

Roughly 80% provide strongly favorable assessments.

The asymmetry in mutual perceptions is striking.

November 22, 2025 at 2:28 AM

🇨🇳➡️🇩🇪 Meanwhile in China:

Chinese respondents express overwhelmingly positive evaluations of German FDI, rating it highly on:

✔️ job creation

✔️ technological upgrading

✔️ national economic development

Roughly 80% provide strongly favorable assessments.

The asymmetry in mutual perceptions is striking.

Chinese respondents express overwhelmingly positive evaluations of German FDI, rating it highly on:

✔️ job creation

✔️ technological upgrading

✔️ national economic development

Roughly 80% provide strongly favorable assessments.

The asymmetry in mutual perceptions is striking.

🧩 Conjoint experiment:

Holding all attributes constant, changing the investor from EU → China reduces selection likelihood by:

➡️ −40 percentage points

Compared with the US:

➡️ −20 points

A substantial origin penalty, independent of project characteristics.

Holding all attributes constant, changing the investor from EU → China reduces selection likelihood by:

➡️ −40 percentage points

Compared with the US:

➡️ −20 points

A substantial origin penalty, independent of project characteristics.

November 22, 2025 at 2:27 AM

🧩 Conjoint experiment:

Holding all attributes constant, changing the investor from EU → China reduces selection likelihood by:

➡️ −40 percentage points

Compared with the US:

➡️ −20 points

A substantial origin penalty, independent of project characteristics.

Holding all attributes constant, changing the investor from EU → China reduces selection likelihood by:

➡️ −40 percentage points

Compared with the US:

➡️ −20 points

A substantial origin penalty, independent of project characteristics.

🟦 EU FDI

🟧 US FDI

🟥 Chinese FDI

Across every domain we measure —

💼 economic prospects

🏭 employment

🧪 innovation

🏛 political autonomy

a remarkably stable preference hierarchy emerges:

EU > US > China

This structure is consistent and highly robust.

🟧 US FDI

🟥 Chinese FDI

Across every domain we measure —

💼 economic prospects

🏭 employment

🧪 innovation

🏛 political autonomy

a remarkably stable preference hierarchy emerges:

EU > US > China

This structure is consistent and highly robust.

November 22, 2025 at 2:25 AM

🟦 EU FDI

🟧 US FDI

🟥 Chinese FDI

Across every domain we measure —

💼 economic prospects

🏭 employment

🧪 innovation

🏛 political autonomy

a remarkably stable preference hierarchy emerges:

EU > US > China

This structure is consistent and highly robust.

🟧 US FDI

🟥 Chinese FDI

Across every domain we measure —

💼 economic prospects

🏭 employment

🧪 innovation

🏛 political autonomy

a remarkably stable preference hierarchy emerges:

EU > US > China

This structure is consistent and highly robust.

📊 The perception gap:

On average, Germans believe that Chinese firms account for 33% of inward FDI.

The actual figure?

👉 ~1% — a roughly 30-fold overestimation. 😬

By contrast:

• EU FDI is systematically underestimated

• US FDI is perceived relatively accurately

On average, Germans believe that Chinese firms account for 33% of inward FDI.

The actual figure?

👉 ~1% — a roughly 30-fold overestimation. 😬

By contrast:

• EU FDI is systematically underestimated

• US FDI is perceived relatively accurately

November 22, 2025 at 2:23 AM

📊 The perception gap:

On average, Germans believe that Chinese firms account for 33% of inward FDI.

The actual figure?

👉 ~1% — a roughly 30-fold overestimation. 😬

By contrast:

• EU FDI is systematically underestimated

• US FDI is perceived relatively accurately

On average, Germans believe that Chinese firms account for 33% of inward FDI.

The actual figure?

👉 ~1% — a roughly 30-fold overestimation. 😬

By contrast:

• EU FDI is systematically underestimated

• US FDI is perceived relatively accurately

🌍💼 Why this matters:

Germany and China are economically intertwined through bilateral FDI flows, not just trade.

As Figure 1 shows 👇

🇩🇪 German FDI in China has expanded sharply since 2004—reaching nearly 3% of Germany’s GDP-equivalent.

🇨🇳 Chinese FDI in Germany, by contrast, remains very small.

Germany and China are economically intertwined through bilateral FDI flows, not just trade.

As Figure 1 shows 👇

🇩🇪 German FDI in China has expanded sharply since 2004—reaching nearly 3% of Germany’s GDP-equivalent.

🇨🇳 Chinese FDI in Germany, by contrast, remains very small.

November 22, 2025 at 2:20 AM

🌍💼 Why this matters:

Germany and China are economically intertwined through bilateral FDI flows, not just trade.

As Figure 1 shows 👇

🇩🇪 German FDI in China has expanded sharply since 2004—reaching nearly 3% of Germany’s GDP-equivalent.

🇨🇳 Chinese FDI in Germany, by contrast, remains very small.

Germany and China are economically intertwined through bilateral FDI flows, not just trade.

As Figure 1 shows 👇

🇩🇪 German FDI in China has expanded sharply since 2004—reaching nearly 3% of Germany’s GDP-equivalent.

🇨🇳 Chinese FDI in Germany, by contrast, remains very small.

However, at the same time, we do not observe that tax rates (or even military targets) were fine-tuned to respond to local economic shocks, like changes in cash crop prices or a severe drought in 1938.

December 10, 2024 at 5:31 PM

However, at the same time, we do not observe that tax rates (or even military targets) were fine-tuned to respond to local economic shocks, like changes in cash crop prices or a severe drought in 1938.

Accordingly, the colonial authorities exercised caution and moderation in the setting of head tax rates: more affluent districts (closer to seaports, producing cash crops and having a railway line) were set higher rates, while the military target was set only in proportion to local population.

December 10, 2024 at 5:29 PM

Accordingly, the colonial authorities exercised caution and moderation in the setting of head tax rates: more affluent districts (closer to seaports, producing cash crops and having a railway line) were set higher rates, while the military target was set only in proportion to local population.

For head tax levy, we show that spikes in head tax rates statistically significantly increased the likelihood of tax-related conflicts, yet were not associated with conflicts of other motives.

December 10, 2024 at 5:28 PM

For head tax levy, we show that spikes in head tax rates statistically significantly increased the likelihood of tax-related conflicts, yet were not associated with conflicts of other motives.

Resistance to conscription mainly boiled down to individual defiance through absenteeism at the drafting boards, as manifested by relatively high absenteeism rates across colonies.

December 10, 2024 at 5:27 PM

Resistance to conscription mainly boiled down to individual defiance through absenteeism at the drafting boards, as manifested by relatively high absenteeism rates across colonies.

Resistance to conscription mainly boiled down to individual defiance through absenteeism at the drafting boards, as manifested by relatively high absenteeism rates across colonies.

December 10, 2024 at 5:25 PM

Resistance to conscription mainly boiled down to individual defiance through absenteeism at the drafting boards, as manifested by relatively high absenteeism rates across colonies.

Likewise, we find strikingly high compliance with the head tax across all colonies. Even under the most conservative demographic assumptions, the collected head tax revenue consistently exceeded 80% of the theoretical expectation, based on head tax rates and estimates of the eligible population.

December 10, 2024 at 5:24 PM

Likewise, we find strikingly high compliance with the head tax across all colonies. Even under the most conservative demographic assumptions, the collected head tax revenue consistently exceeded 80% of the theoretical expectation, based on head tax rates and estimates of the eligible population.

Our findings reveal that colonial coercion was highly effective. First of all, military recruitment targets were nearly always met, with the mean Military Enforcement Rate standing at 99.4%!

December 10, 2024 at 5:23 PM

Our findings reveal that colonial coercion was highly effective. First of all, military recruitment targets were nearly always met, with the mean Military Enforcement Rate standing at 99.4%!

To do so, we undertook extensive digitization efforts and created a unique district-level panel dataset covering military conscription and head tax levies for every year from 1919 to 1949, for all eight colonies in French West Africa (example of conscription table below).

December 10, 2024 at 5:22 PM

To do so, we undertook extensive digitization efforts and created a unique district-level panel dataset covering military conscription and head tax levies for every year from 1919 to 1949, for all eight colonies in French West Africa (example of conscription table below).

We contribute to this debate by looking at two pillars of colonial rule in French West Africa: head tax collection and military conscription.

December 10, 2024 at 5:20 PM

We contribute to this debate by looking at two pillars of colonial rule in French West Africa: head tax collection and military conscription.

Such status quo playing (choice reluctance) is more pronounced among the Chinese respondents from working-class or farming families, and significantly less visible among individuals with family backgrounds in the private sector. The same heterogeneity doesn’t exist for the French sample.

November 27, 2024 at 6:21 PM

Such status quo playing (choice reluctance) is more pronounced among the Chinese respondents from working-class or farming families, and significantly less visible among individuals with family backgrounds in the private sector. The same heterogeneity doesn’t exist for the French sample.

In regression terms, the significant merit-luck gap starts to appear for the Chinese sample when we either exclude only the status-quo distributions, or all status-quo players from the sample.

November 27, 2024 at 6:20 PM

In regression terms, the significant merit-luck gap starts to appear for the Chinese sample when we either exclude only the status-quo distributions, or all status-quo players from the sample.

But! When we remove the status quo players from the sample, Chinese respondents who do not play status quo (i.e., those who make an active choice) display a significant merit-luck gap in their redistribution decisions. The non-status-quo-playing Chinese are as meritocratic as the French!

November 27, 2024 at 6:15 PM

But! When we remove the status quo players from the sample, Chinese respondents who do not play status quo (i.e., those who make an active choice) display a significant merit-luck gap in their redistribution decisions. The non-status-quo-playing Chinese are as meritocratic as the French!

Furthermore, Chinese respondents do not redistribute more to the worker who lost out in the luck scenario than in the merit scenario, across both status quo treatments, confirming previous findings that they do appear unmeritocratic in the aggregate, while the French are consistently meritocratic.

November 27, 2024 at 6:14 PM

Furthermore, Chinese respondents do not redistribute more to the worker who lost out in the luck scenario than in the merit scenario, across both status quo treatments, confirming previous findings that they do appear unmeritocratic in the aggregate, while the French are consistently meritocratic.

We indeed confirm our hypothesis: Compared to French respondents (colored in blue), Chinese respondents (colored in red) consistently and significantly choose more non-redistribution (dotted line) across both highly unequal (12/0 split) and relatively equal status quo (7/5 split) treatments.

November 27, 2024 at 6:12 PM

We indeed confirm our hypothesis: Compared to French respondents (colored in blue), Chinese respondents (colored in red) consistently and significantly choose more non-redistribution (dotted line) across both highly unequal (12/0 split) and relatively equal status quo (7/5 split) treatments.

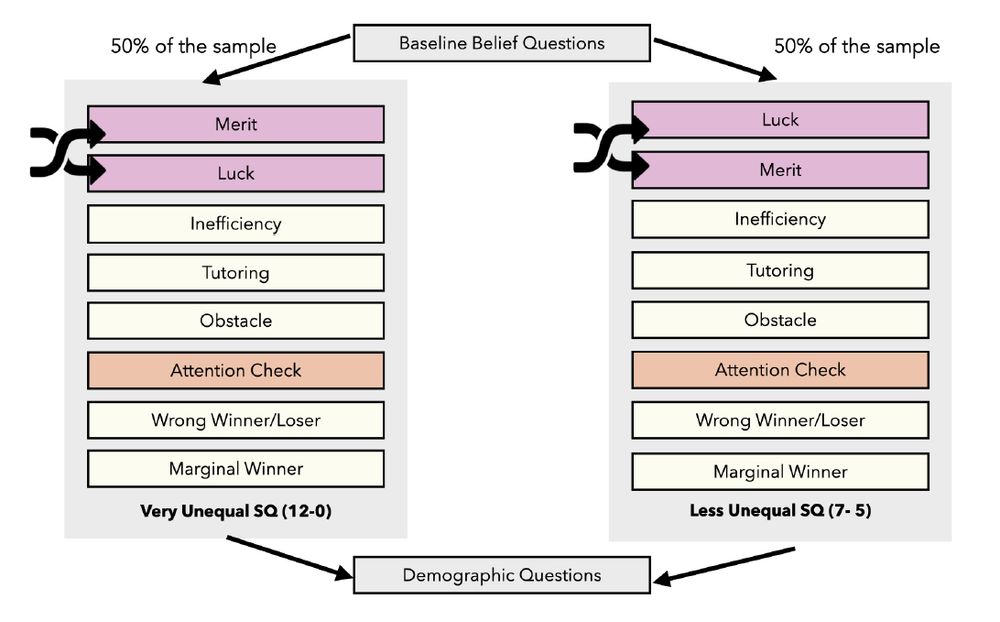

We also augment the luck scenarios commonly used in third-party spectator games by introducing additional dimensions of inequality of opportunities, such as head starts, obstacles, Type I and Type II errors, as well as marginal winners.

November 27, 2024 at 6:10 PM

We also augment the luck scenarios commonly used in third-party spectator games by introducing additional dimensions of inequality of opportunities, such as head starts, obstacles, Type I and Type II errors, as well as marginal winners.

We run a third-party spectator game with elite university students in China and France, by varying the initial split of payoffs between two real-life workers to redistribute from, i.e., either the respondent is assigned to an equal status quo (7/5), or unequal status quo (12/0) scenario.

November 27, 2024 at 6:09 PM

We run a third-party spectator game with elite university students in China and France, by varying the initial split of payoffs between two real-life workers to redistribute from, i.e., either the respondent is assigned to an equal status quo (7/5), or unequal status quo (12/0) scenario.