Julie Zhiyu Fu

@zhiyufu.bsky.social

finance AP @WUSTLbusiness | International Macro Finance| Asset Pricing

Our take: if you believe investors are heterogeneous, quantity data cannot be ignored.

Paper: priceimpactbound.github.io/PriceImpactB...

Paper: priceimpactbound.github.io/PriceImpactB...

September 22, 2025 at 3:27 PM

Our take: if you believe investors are heterogeneous, quantity data cannot be ignored.

Paper: priceimpactbound.github.io/PriceImpactB...

Paper: priceimpactbound.github.io/PriceImpactB...

Finally, why does the "inelasticity" debate matter?

It's not just a number—it's about whether we can understand asset prices using quantity data.

elastic market → quantities are a sideshow, price data are all you need

inelastic → quantities are CENTRAL for prices

It's not just a number—it's about whether we can understand asset prices using quantity data.

elastic market → quantities are a sideshow, price data are all you need

inelastic → quantities are CENTRAL for prices

September 22, 2025 at 3:27 PM

Finally, why does the "inelasticity" debate matter?

It's not just a number—it's about whether we can understand asset prices using quantity data.

elastic market → quantities are a sideshow, price data are all you need

inelastic → quantities are CENTRAL for prices

It's not just a number—it's about whether we can understand asset prices using quantity data.

elastic market → quantities are a sideshow, price data are all you need

inelastic → quantities are CENTRAL for prices

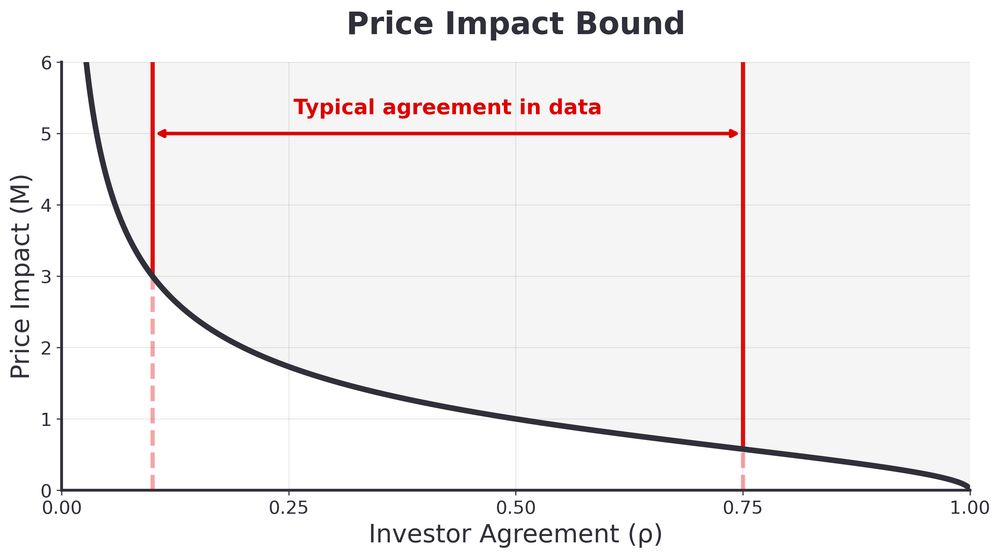

For avg stocks, the price impact bound ≈ 1 with a medium level of agreement (consistent with data).

To argue for a price impact less than 0.1, you really need investors to agree with each other for more than 99%!

To argue for a price impact less than 0.1, you really need investors to agree with each other for more than 99%!

September 22, 2025 at 3:27 PM

For avg stocks, the price impact bound ≈ 1 with a medium level of agreement (consistent with data).

To argue for a price impact less than 0.1, you really need investors to agree with each other for more than 99%!

To argue for a price impact less than 0.1, you really need investors to agree with each other for more than 99%!

We formalize this intuition mathematically in a simple bound:

Price Impact ≥ (σ_p/σ_q) × √(1/ρ - 1)

where agreement ρ can be loosely understood as avg. corr across investors.

The bound needs few structural assumptions, just like the Hansen–Jagannathan bound for SDF

Price Impact ≥ (σ_p/σ_q) × √(1/ρ - 1)

where agreement ρ can be loosely understood as avg. corr across investors.

The bound needs few structural assumptions, just like the Hansen–Jagannathan bound for SDF

September 22, 2025 at 3:27 PM

We formalize this intuition mathematically in a simple bound:

Price Impact ≥ (σ_p/σ_q) × √(1/ρ - 1)

where agreement ρ can be loosely understood as avg. corr across investors.

The bound needs few structural assumptions, just like the Hansen–Jagannathan bound for SDF

Price Impact ≥ (σ_p/σ_q) × √(1/ρ - 1)

where agreement ρ can be loosely understood as avg. corr across investors.

The bound needs few structural assumptions, just like the Hansen–Jagannathan bound for SDF

It has to be that even though they disagree on what the right price should be, their demand is inelastic to price changes.

→ A small portfolio flow requires a large price adjustment to clear

→ A small portfolio flow requires a large price adjustment to clear

September 22, 2025 at 3:27 PM

It has to be that even though they disagree on what the right price should be, their demand is inelastic to price changes.

→ A small portfolio flow requires a large price adjustment to clear

→ A small portfolio flow requires a large price adjustment to clear

The argument rests on a simple observation: asset prices are volatile, yet portfolio flows are small.

You can easily generate little trading alongside volatile prices with large agreement.

But with large disagreement and volatile prices, why don't investors trade more?

You can easily generate little trading alongside volatile prices with large agreement.

But with large disagreement and volatile prices, why don't investors trade more?

September 22, 2025 at 3:27 PM

The argument rests on a simple observation: asset prices are volatile, yet portfolio flows are small.

You can easily generate little trading alongside volatile prices with large agreement.

But with large disagreement and volatile prices, why don't investors trade more?

You can easily generate little trading alongside volatile prices with large agreement.

But with large disagreement and volatile prices, why don't investors trade more?

Our take: if you believe investors are heterogeneous, quantity data cannot be ignored.

Paper: priceimpactbound.github.io/PriceImpactB...

Paper: priceimpactbound.github.io/PriceImpactB...

September 21, 2025 at 2:35 PM

Our take: if you believe investors are heterogeneous, quantity data cannot be ignored.

Paper: priceimpactbound.github.io/PriceImpactB...

Paper: priceimpactbound.github.io/PriceImpactB...

Finally, why does the "inelasticity" debate matter?

It's not just a number—it's about whether we can understand asset prices using quantity data.

elastic market → quantities are a sideshow, price data are all you need

inelastic → quantities are CENTRAL for prices

It's not just a number—it's about whether we can understand asset prices using quantity data.

elastic market → quantities are a sideshow, price data are all you need

inelastic → quantities are CENTRAL for prices

September 21, 2025 at 2:35 PM

Finally, why does the "inelasticity" debate matter?

It's not just a number—it's about whether we can understand asset prices using quantity data.

elastic market → quantities are a sideshow, price data are all you need

inelastic → quantities are CENTRAL for prices

It's not just a number—it's about whether we can understand asset prices using quantity data.

elastic market → quantities are a sideshow, price data are all you need

inelastic → quantities are CENTRAL for prices

For avg stocks, the price impact bound ≈ 1 with a medium level of agreement (consistent with data).

To argue for a price impact less than 0.1, you really need investors to agree with each other for more than 99%!

To argue for a price impact less than 0.1, you really need investors to agree with each other for more than 99%!

September 21, 2025 at 2:35 PM

For avg stocks, the price impact bound ≈ 1 with a medium level of agreement (consistent with data).

To argue for a price impact less than 0.1, you really need investors to agree with each other for more than 99%!

To argue for a price impact less than 0.1, you really need investors to agree with each other for more than 99%!

We formalize this intuition mathematically in a simple bound:

Price Impact ≥ (σ_p/σ_q) × √(1/ρ - 1)

where agreement ρ can be loosely understood as avg. corr across investors.

The bound needs few structural assumptions, just like the Hansen–Jagannathan bound for SDF

Price Impact ≥ (σ_p/σ_q) × √(1/ρ - 1)

where agreement ρ can be loosely understood as avg. corr across investors.

The bound needs few structural assumptions, just like the Hansen–Jagannathan bound for SDF

September 21, 2025 at 2:35 PM

We formalize this intuition mathematically in a simple bound:

Price Impact ≥ (σ_p/σ_q) × √(1/ρ - 1)

where agreement ρ can be loosely understood as avg. corr across investors.

The bound needs few structural assumptions, just like the Hansen–Jagannathan bound for SDF

Price Impact ≥ (σ_p/σ_q) × √(1/ρ - 1)

where agreement ρ can be loosely understood as avg. corr across investors.

The bound needs few structural assumptions, just like the Hansen–Jagannathan bound for SDF

It has to be that even though they disagree on what the right price should be, their demand is inelastic to price changes.

→ A small portfolio flow requires a large price adjustment to clear

→ A small portfolio flow requires a large price adjustment to clear

September 21, 2025 at 2:35 PM

It has to be that even though they disagree on what the right price should be, their demand is inelastic to price changes.

→ A small portfolio flow requires a large price adjustment to clear

→ A small portfolio flow requires a large price adjustment to clear

The argument rests on a simple observation: asset prices are volatile, yet portfolio flows are small.

You can easily generate little trading alongside volatile prices with large agreement.

But with large disagreement and volatile prices, why don't investors trade more?

You can easily generate little trading alongside volatile prices with large agreement.

But with large disagreement and volatile prices, why don't investors trade more?

September 21, 2025 at 2:35 PM

The argument rests on a simple observation: asset prices are volatile, yet portfolio flows are small.

You can easily generate little trading alongside volatile prices with large agreement.

But with large disagreement and volatile prices, why don't investors trade more?

You can easily generate little trading alongside volatile prices with large agreement.

But with large disagreement and volatile prices, why don't investors trade more?

This makes the basis trade unwinding explanation really unsatisfying to me...can anyone with more institutional knowledge explain to me why this may also happen due to basis trade unwinding?

April 9, 2025 at 4:15 PM

This makes the basis trade unwinding explanation really unsatisfying to me...can anyone with more institutional knowledge explain to me why this may also happen due to basis trade unwinding?

Most curious about 4 and in particular on how to use Git with different type of co-authors: who I can't force to use Git and who can use it minimally.

December 19, 2024 at 10:19 PM

Most curious about 4 and in particular on how to use Git with different type of co-authors: who I can't force to use Git and who can use it minimally.

Please send comments and happy to discuss more :)

SSRN: papers.ssrn.com/sol3/papers....

SSRN: papers.ssrn.com/sol3/papers....

Anatomy of the Treasury Market: Who Moves Yields?

We develop a quantity-based framework to study the drivers of U.S. Treasury yields. Our method allows for flexible identification of price and factor sensitivit

papers.ssrn.com

November 27, 2024 at 9:33 PM

Please send comments and happy to discuss more :)

SSRN: papers.ssrn.com/sol3/papers....

SSRN: papers.ssrn.com/sol3/papers....

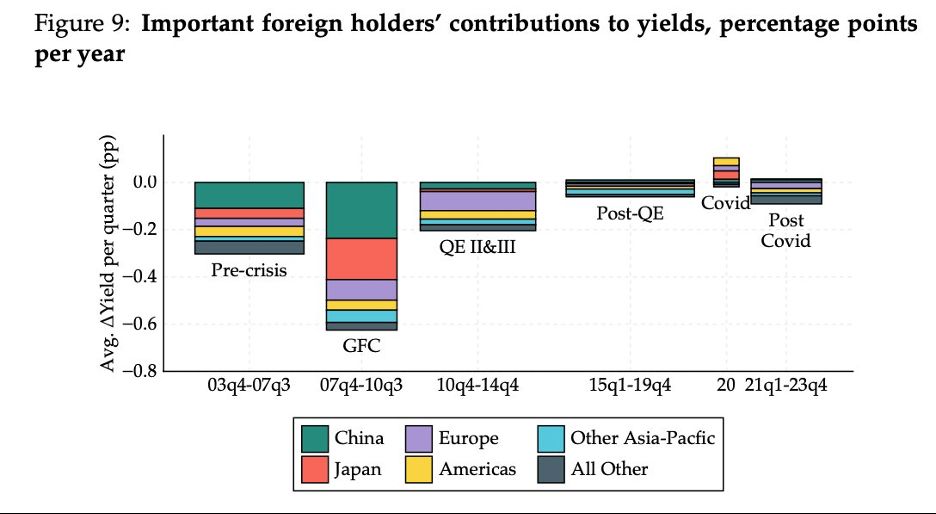

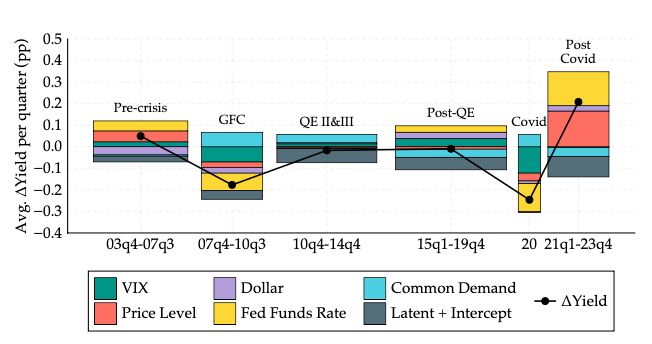

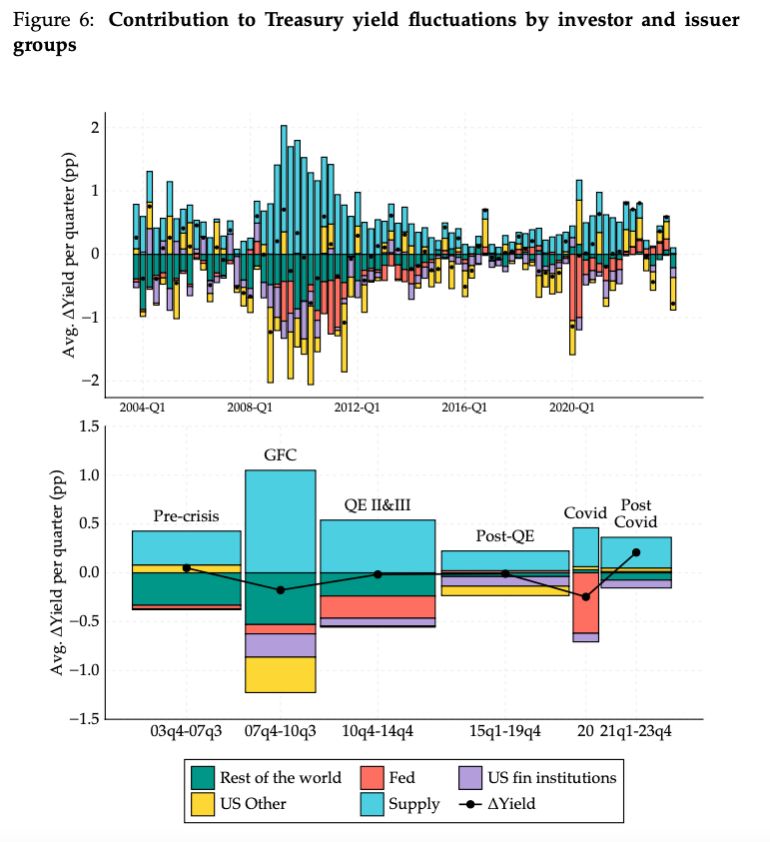

4.3/ Finally, the idea that a Treasury sell-off by major foreign investors such as China may have strong yield-increasing effect is quite correct in the first decade of the 2000s but less so in recent years -- foreign investors do not contribute much to yield movements since 2015.

November 27, 2024 at 9:33 PM

4.3/ Finally, the idea that a Treasury sell-off by major foreign investors such as China may have strong yield-increasing effect is quite correct in the first decade of the 2000s but less so in recent years -- foreign investors do not contribute much to yield movements since 2015.

4.2/ U.S. banks and foreign investors become substantially more price inelastic after the GFC, while the Fed has stepped up to the game as a state-contingent liquidity provider in the Treasury market. We discuss factors contributing to these regime shifts in detail in the paper.

November 27, 2024 at 9:33 PM

4.2/ U.S. banks and foreign investors become substantially more price inelastic after the GFC, while the Fed has stepped up to the game as a state-contingent liquidity provider in the Treasury market. We discuss factors contributing to these regime shifts in detail in the paper.

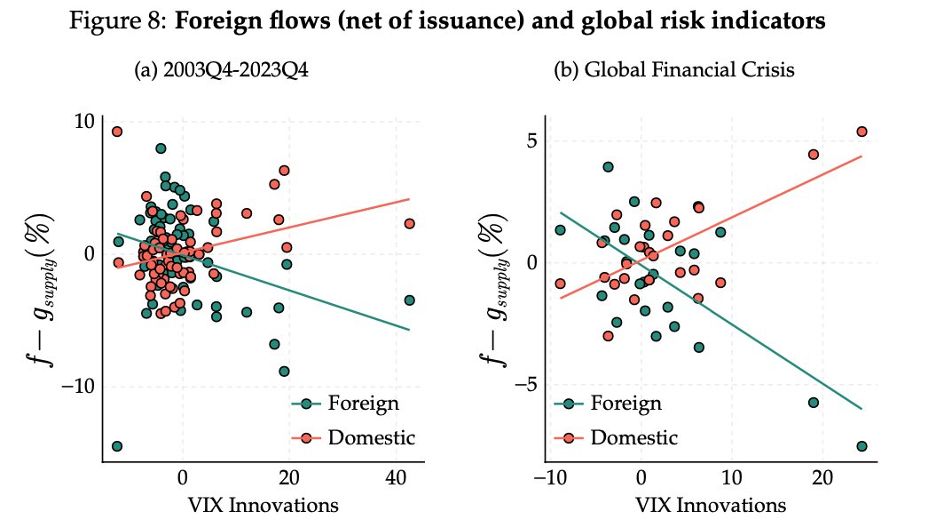

4.1/ We find little evidence supporting the conventional wisdom that foreigners are the major driver of "flight-to-Treasuries" during risk-off episodes. The pattern is evident even in the raw data, and with our model we can quantify the respective role of foreign & domestic investors.

November 27, 2024 at 9:33 PM

4.1/ We find little evidence supporting the conventional wisdom that foreigners are the major driver of "flight-to-Treasuries" during risk-off episodes. The pattern is evident even in the raw data, and with our model we can quantify the respective role of foreign & domestic investors.

4/ We can use the estimated system to decompose yield movements and study who and what factors move yields. Then we focus on several important investor groups and discuss three main findings:

November 27, 2024 at 9:33 PM

4/ We can use the estimated system to decompose yield movements and study who and what factors move yields. Then we focus on several important investor groups and discuss three main findings:

3/ The estimated "macro" multiplier is 1 -- 1% positive demand shocks push down yields on a 10-year note by 10bps. This aligns well with estimates in the literature: larger than "micro" multipliers for govt bonds but smaller than the macro multiplier for stocks.

November 27, 2024 at 9:33 PM

3/ The estimated "macro" multiplier is 1 -- 1% positive demand shocks push down yields on a 10-year note by 10bps. This aligns well with estimates in the literature: larger than "micro" multipliers for govt bonds but smaller than the macro multiplier for stocks.