Christian Julliard

@christianjulliard.net

I think, read, write, teach (and take photos). Associate Professor @LSEFinance. I study the interaction between financial markets and the macroeconomy.

https://christianjulliard.net

https://christianjulliard.net

What about time-varying risk premia?

Contrary to many models, we find no evidence that stochastic volatilities in consumption drive them.

Instead, it’s the (shocks to the) conditional mean of consumption the main link between consumption and returns.

11/n

11/n

June 17, 2025 at 10:04 PM

What about time-varying risk premia?

Contrary to many models, we find no evidence that stochastic volatilities in consumption drive them.

Instead, it’s the (shocks to the) conditional mean of consumption the main link between consumption and returns.

11/n

11/n

We verify these mechanisms with a plethora of perturbations to specification / data / frequencies / etc

No matter how we slice it, the result holds: consumption reacts slowly but strongly to financial shocks, & these slowly propagating shocks command very large risk premia.

10/n

No matter how we slice it, the result holds: consumption reacts slowly but strongly to financial shocks, & these slowly propagating shocks command very large risk premia.

10/n

June 17, 2025 at 10:04 PM

We verify these mechanisms with a plethora of perturbations to specification / data / frequencies / etc

No matter how we slice it, the result holds: consumption reacts slowly but strongly to financial shocks, & these slowly propagating shocks command very large risk premia.

10/n

No matter how we slice it, the result holds: consumption reacts slowly but strongly to financial shocks, & these slowly propagating shocks command very large risk premia.

10/n

Is this Long Run Risk?

Not verbatim, but rather medium run / business cycle risk: consumption reacts to priced shocks fully within 2-3 years.

Hence, priced consumption risk is about what happens within the next business cycle, rather than hundred years down the line.

9/n

Not verbatim, but rather medium run / business cycle risk: consumption reacts to priced shocks fully within 2-3 years.

Hence, priced consumption risk is about what happens within the next business cycle, rather than hundred years down the line.

9/n

June 17, 2025 at 10:04 PM

Is this Long Run Risk?

Not verbatim, but rather medium run / business cycle risk: consumption reacts to priced shocks fully within 2-3 years.

Hence, priced consumption risk is about what happens within the next business cycle, rather than hundred years down the line.

9/n

Not verbatim, but rather medium run / business cycle risk: consumption reacts to priced shocks fully within 2-3 years.

Hence, priced consumption risk is about what happens within the next business cycle, rather than hundred years down the line.

9/n

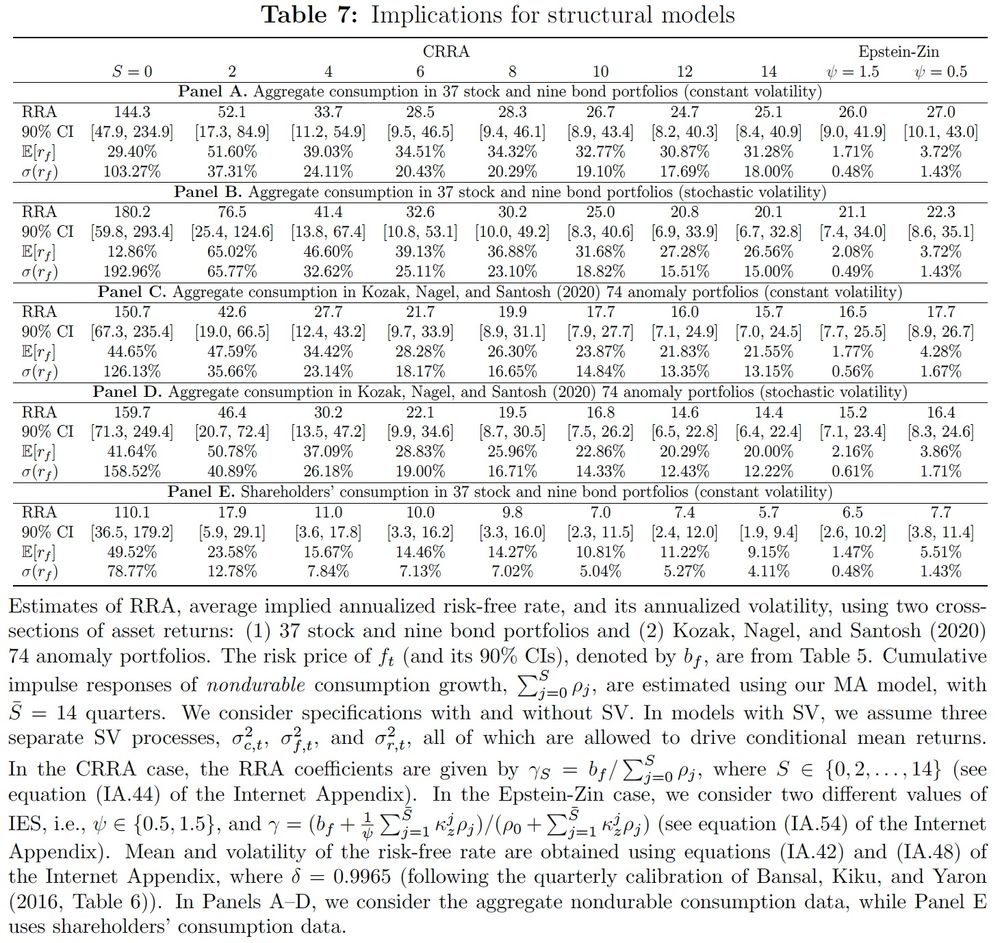

We embed our estimated process into a standard recursive utility model.

With low risk aversion, it explains both the equity premium and the risk-free rate puzzles.

No need for exotic preferences or extreme calibrations.

8/n

8/n

June 17, 2025 at 10:04 PM

We embed our estimated process into a standard recursive utility model.

With low risk aversion, it explains both the equity premium and the risk-free rate puzzles.

No need for exotic preferences or extreme calibrations.

8/n

8/n

To validate our identification, we turn to micro data.

Only stockholders’ consumption responds to financial shocks.

Non-stockholders’ doesn’t. Aggregate consumption sits in between.

Exactly what theory predicts.

7/n

7/n

June 17, 2025 at 10:04 PM

To validate our identification, we turn to micro data.

Only stockholders’ consumption responds to financial shocks.

Non-stockholders’ doesn’t. Aggregate consumption sits in between.

Exactly what theory predicts.

7/n

7/n

These shocks aren’t just statistically significant—they’re economically meaningful. They command an annual Sharpe ratio of ~0.5 (as large as the market!) and explain a large share of stock return variation (and a modest but significant share of bond excess returns too).

6/n

6/n

June 17, 2025 at 10:04 PM

These shocks aren’t just statistically significant—they’re economically meaningful. They command an annual Sharpe ratio of ~0.5 (as large as the market!) and explain a large share of stock return variation (and a modest but significant share of bond excess returns too).

6/n

6/n

Using a flexible state-space model we find that aggregate consumption reacts over multiple quarters to shocks spanned by financial markets, accounting for over 25% of consumption variation.

5/n

5/n

June 17, 2025 at 10:04 PM

Using a flexible state-space model we find that aggregate consumption reacts over multiple quarters to shocks spanned by financial markets, accounting for over 25% of consumption variation.

5/n

5/n

🚨 "Consumption in Asset Returns" (w. Svetlana Bryzgalova

& Jiantao Huang) forthcoming @ Journal of Finance

We use asset returns to uncover the elusive dynamics of consumption.

Turns out, financial markets know a lot about future consumption—and it matters for both macro & asset pricing

🧵👇 1/n

& Jiantao Huang) forthcoming @ Journal of Finance

We use asset returns to uncover the elusive dynamics of consumption.

Turns out, financial markets know a lot about future consumption—and it matters for both macro & asset pricing

🧵👇 1/n

June 17, 2025 at 10:04 PM

🚨 "Consumption in Asset Returns" (w. Svetlana Bryzgalova

& Jiantao Huang) forthcoming @ Journal of Finance

We use asset returns to uncover the elusive dynamics of consumption.

Turns out, financial markets know a lot about future consumption—and it matters for both macro & asset pricing

🧵👇 1/n

& Jiantao Huang) forthcoming @ Journal of Finance

We use asset returns to uncover the elusive dynamics of consumption.

Turns out, financial markets know a lot about future consumption—and it matters for both macro & asset pricing

🧵👇 1/n

(Marketing with?) fear of a run

April 3, 2025 at 4:25 PM

(Marketing with?) fear of a run

If I had not cancelled already my monthly donation to @theguardian.com because of the economic illiteracy of their editorial team, this attack on central bank independence would have been the last straw

March 30, 2025 at 3:24 PM

If I had not cancelled already my monthly donation to @theguardian.com because of the economic illiteracy of their editorial team, this attack on central bank independence would have been the last straw

UK used car price trends are quite telling:

March 16, 2025 at 10:56 PM

UK used car price trends are quite telling:

👇A financial economist to follow.

@alex-dickerson.bsky.social

Producer of great public goods for corporate bond research at openbondassetpricing.com

@alex-dickerson.bsky.social

Producer of great public goods for corporate bond research at openbondassetpricing.com

November 23, 2024 at 10:52 AM

👇A financial economist to follow.

@alex-dickerson.bsky.social

Producer of great public goods for corporate bond research at openbondassetpricing.com

@alex-dickerson.bsky.social

Producer of great public goods for corporate bond research at openbondassetpricing.com

A bit of a "Death Start" too ;-)

and much better in motion: tinyurl.com/554v4tn9

and much better in motion: tinyurl.com/554v4tn9

November 13, 2024 at 12:01 PM

A bit of a "Death Start" too ;-)

and much better in motion: tinyurl.com/554v4tn9

and much better in motion: tinyurl.com/554v4tn9

Why BFM? Unlike traditional methods, BFM provides valid credible intervals and detects weakly identified factors, making it robust yet intuitive.

3/n #AssetPricing

3/n #AssetPricing

October 19, 2024 at 11:46 AM

Why BFM? Unlike traditional methods, BFM provides valid credible intervals and detects weakly identified factors, making it robust yet intuitive.

3/n #AssetPricing

3/n #AssetPricing

🚨New (very short) paper alert:

"Bayesian Fama-MacBeth Regressions" with @SBryzgalova and Jiantao Huang tinyurl.com/bddpezz6

🧵1/n #Finance #Econometrics

"Bayesian Fama-MacBeth Regressions" with @SBryzgalova and Jiantao Huang tinyurl.com/bddpezz6

🧵1/n #Finance #Econometrics

October 19, 2024 at 11:45 AM

🚨New (very short) paper alert:

"Bayesian Fama-MacBeth Regressions" with @SBryzgalova and Jiantao Huang tinyurl.com/bddpezz6

🧵1/n #Finance #Econometrics

"Bayesian Fama-MacBeth Regressions" with @SBryzgalova and Jiantao Huang tinyurl.com/bddpezz6

🧵1/n #Finance #Econometrics